0 DTE.

They have taken the world by storm and transformed the market’s landscape forever.

Some say they've broken the VIX. That's up for debate.

Others claim they'll cause the next black swan event, wiping out 30% of the markets in a single day. But you could say the same about pretty much any financial innovation.

And then there are those who believe that with the right framework, discipline, and maybe a little luck, trading 0 DTEs can make you rich overnight.

We've heard that before but have yet to see it become a reality for retail traders.

Until now, there was nothing new under the sun. Finance introduced a new product that many don't fully grasp. Everyone understands that a 0 DTE, or a daily contract, expires any day of the week, unlike weeklies, which expire once a week on Fridays.

However, few understand their utility and may dismiss them prematurely while they're still in their infancy.

Cue the raised eyebrows: Utility? What sort of utility could this product possibly have? Isn't it just another tool for transferring money from gambling retail traders straight into Ken's pocket? Yes and no.

If 0 DTEs weren't useful to the big hands on Wall Street, they wouldn't account for half of the daily options volume. For starters, they're cheap and super easy to manage. No strings attached: you buy them today, and they're gone by tomorrow.

But just how useful is that?

Well, let's dive again into the world of fund managers, traders, and anyone who manages a book.

The overnight trade has some long periods of rangebound.

At first glance, this chart might not seem very informative. However, something immediately caught our attention: the best time to sell 0 DTE options overnight was in early 2022. It's hard to forget that period—the beginning of the war in Ukraine and Jay Powell's fast and furious race against inflation. Let's just say markets were a bit unsettled.

This is quite peculiar. Normally, boring is good for business when you're on the short side, and you tend to close up shop when there's too much risk in the market.

Last week was another prime example: when VVIX moved up 10%, we were the first to scale back our positions, unwilling to take on potential overnight risk.

This is incredibly helpful in refining our hypothesis: could it be that during market turbulence, the overnight hedging flow faces a smaller supply and, consequently, distorts the prices of 0 DTE options?

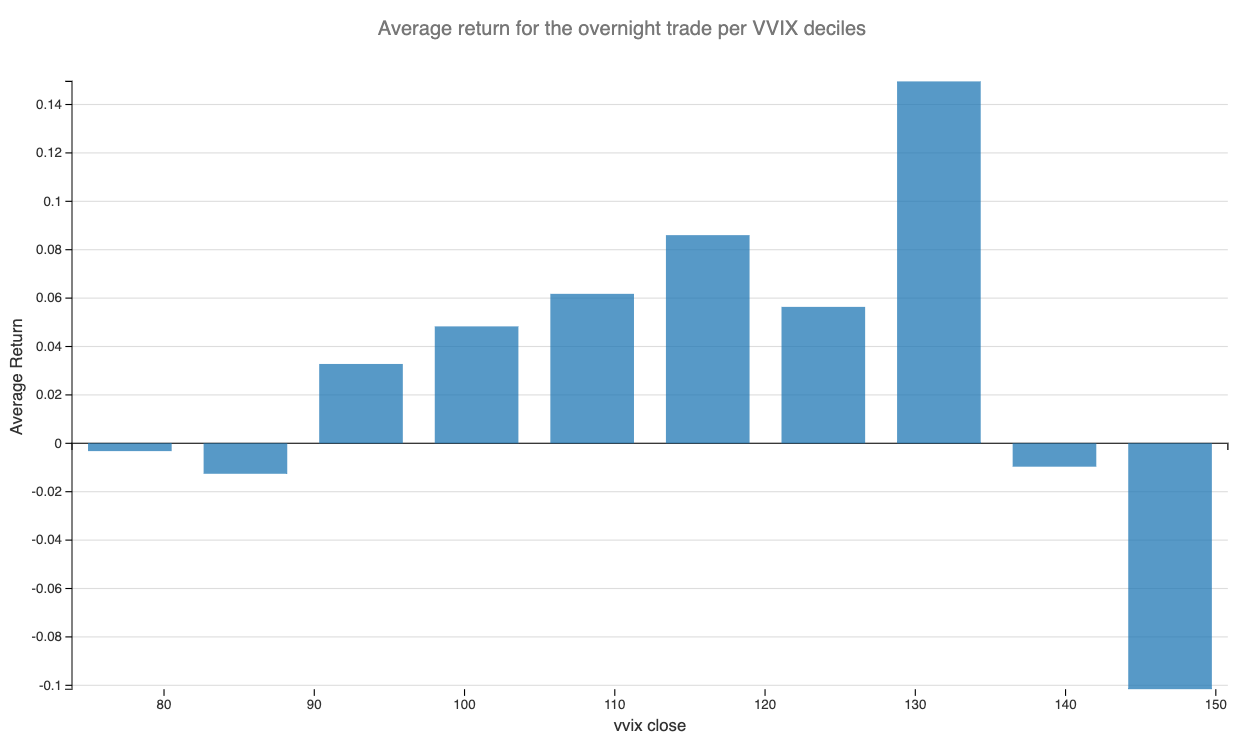

Let's test this hypothesis using VVIX as a filter.

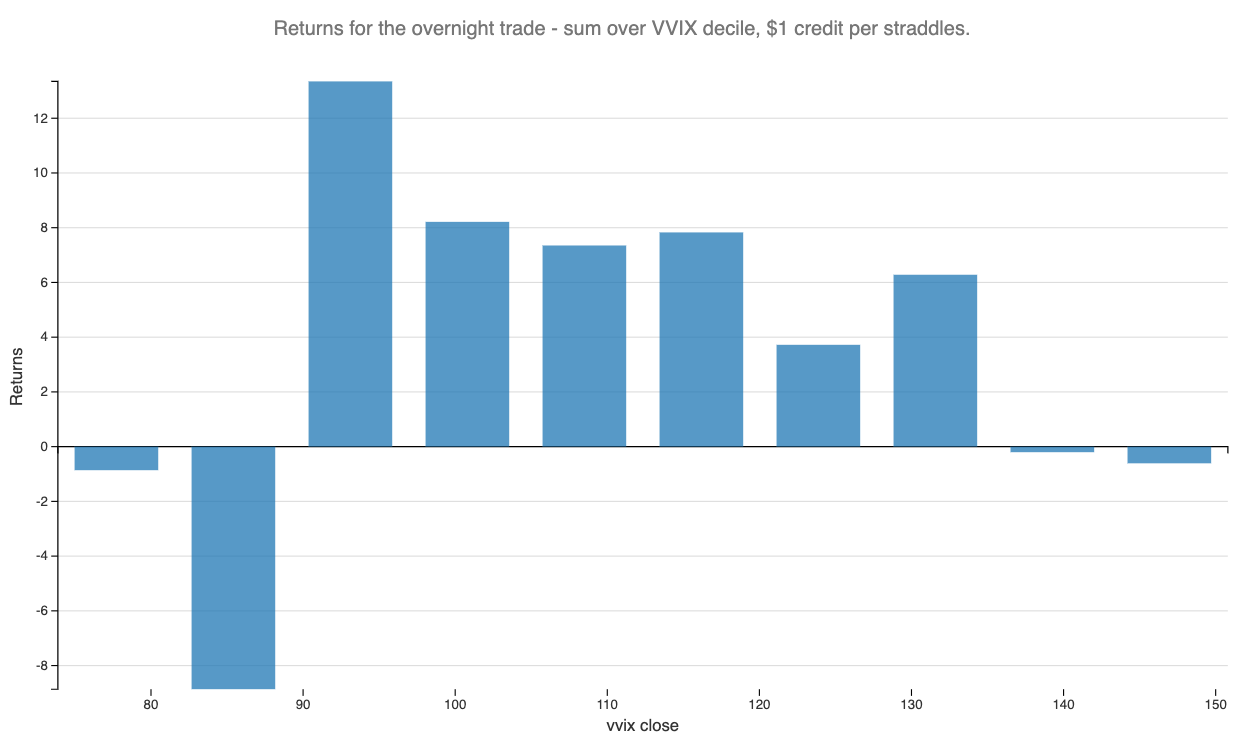

There's something quite striking here. The average return is almost perfectly linear between VVIX levels of 80 to 130. Let's look at the sum of PnL, which will consider the number of occurrences.

Thank you for reading Sharpe Two. This post is public so feel free to share it.

Finding uncomfortable yet very profitable edges.

On average, VVIX hovers around 90 and rarely spends much time above 110. When selling options, a commonly accepted risk management threshold is to start viewing things differently when VVIX surpasses 100.

As it turns out, you might want to scale down on longer-dated options and instead focus on the ultra-short-dated ones during these periods.

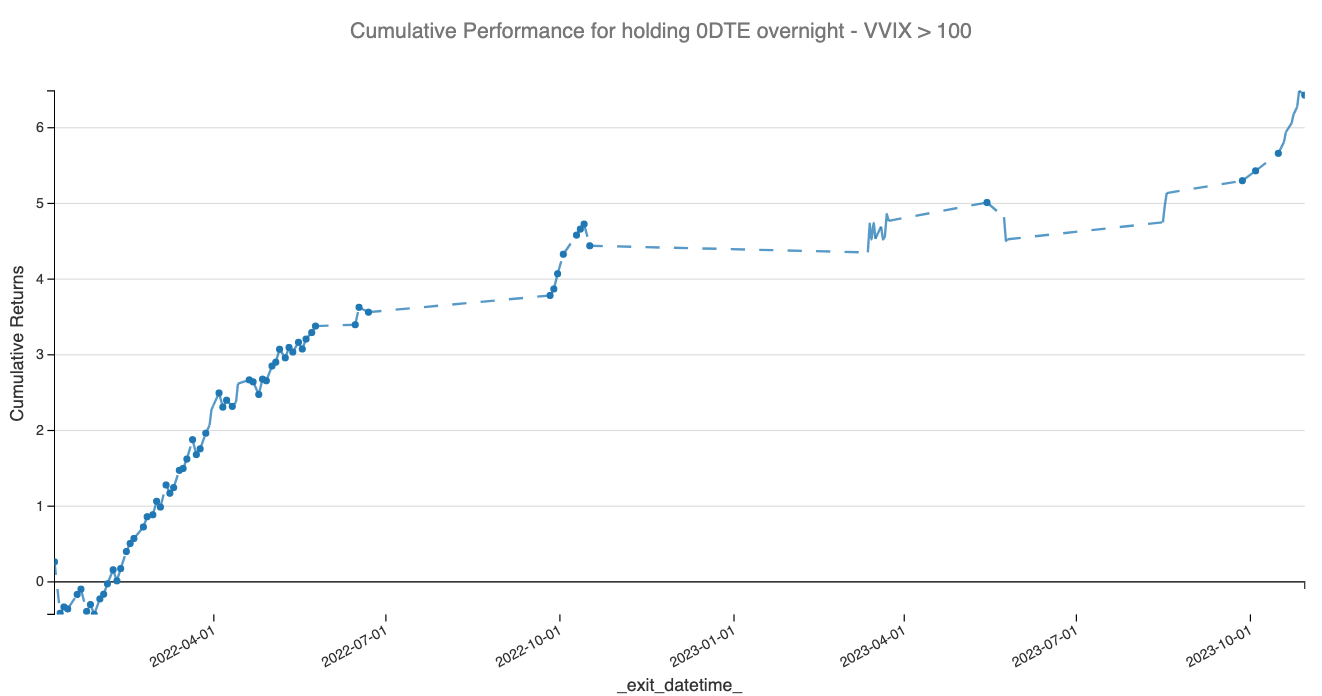

So, let's examine the cumulative PnL if we were to enter this trade only when VVIX was above 100.

This already looks much more promising. We've indeed captured most of our initial observations, and we can see that overall, most periods of turmoil were positive.

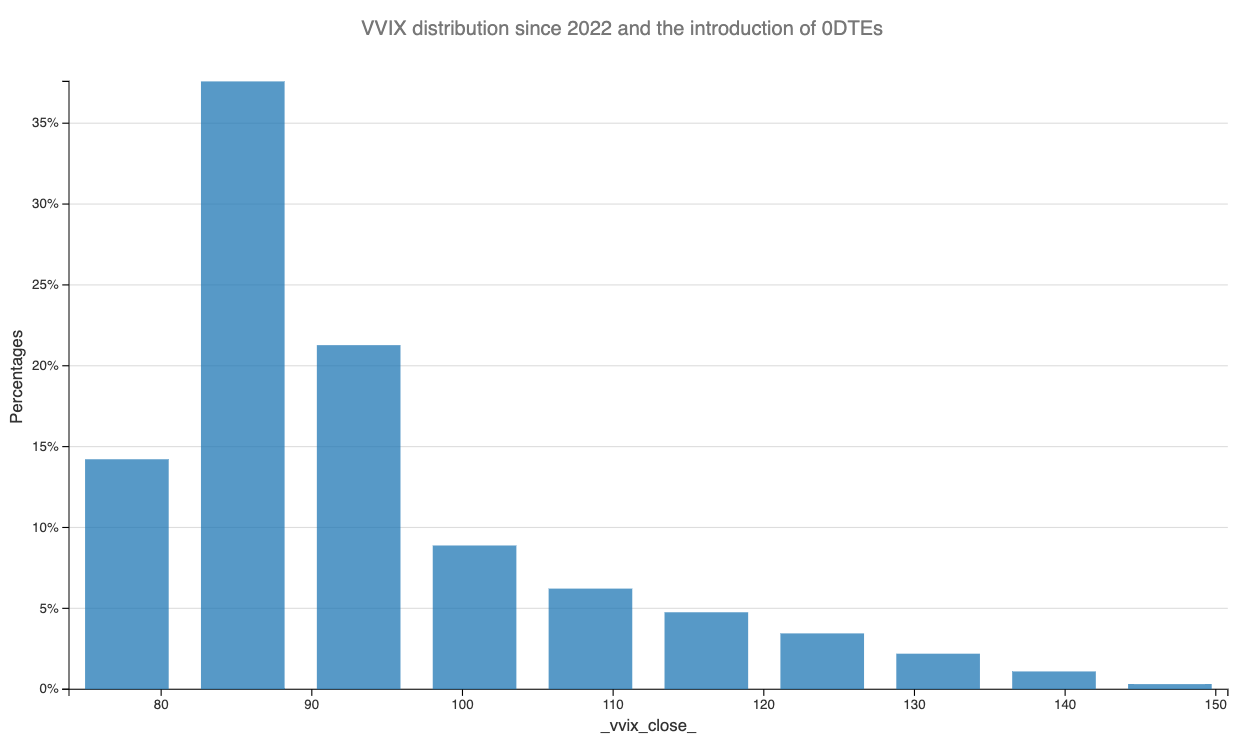

The issue with this approach is that it filters out many signals. The distribution of VVIX in 2022 isn't too different from its distribution since 2007, and it only spends less than 80% of the time above 100.

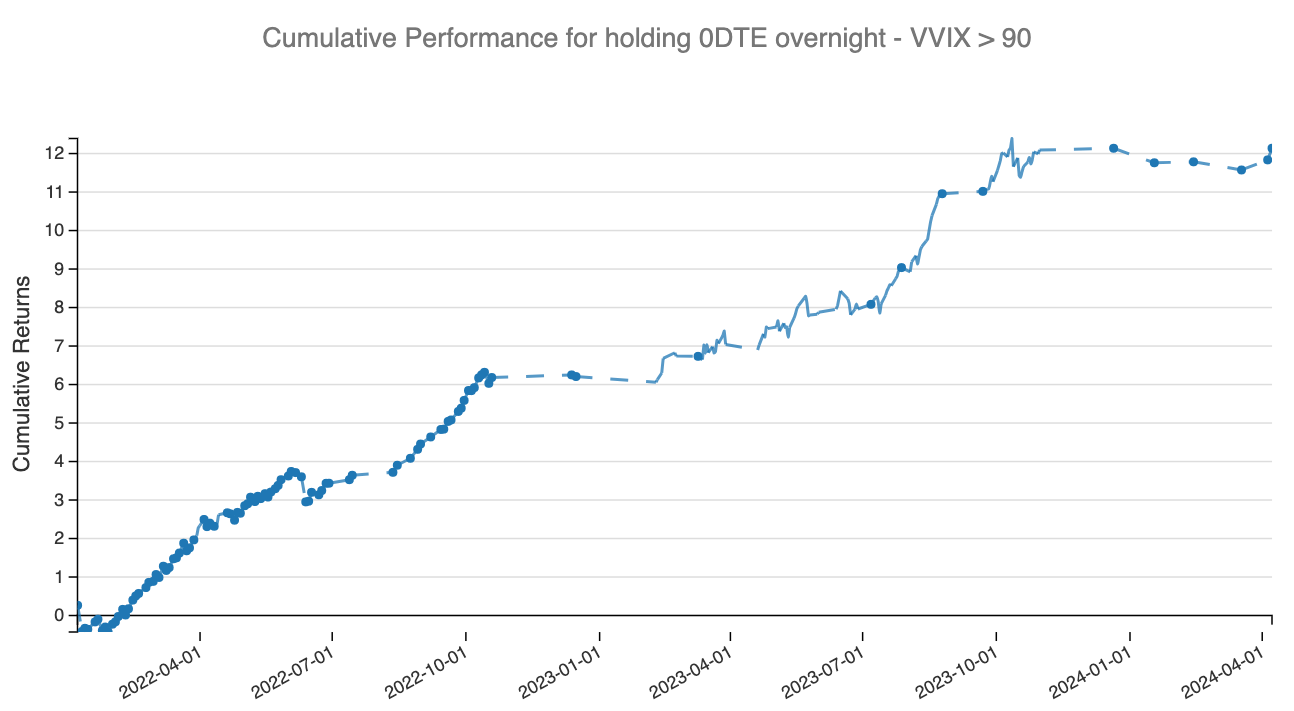

So, what happens if we're willing to accept a slightly higher level of risk and look to implement this trade as soon as VVIX rises above its historical average?

This becomes a trade that's hard to ignore, as every "crisis" over the past two years has shown a clear path to profitability for those willing to take on that overnight risk.

Now, a few words of caution. To our knowledge, this is the first documented study of the overnight effect in 0 DTE options. You might want to wait for academia to develop more scientific and robust testing methods. The closest thing we could think of was the Weekend Trade documented in Positional Option Trading by Dr. Sinclair.

In full disclosure, we all agree that more digging will be required. However, it's good enough for us traders, and we'll start trading it. But you shouldn't take this (or anything we publish) as financial advice.

The dataset is still relatively small (1,913 trades across eight tickers, mainly indices) since January 2022, and we may not have seen the event that could wipe out this strategy in a single day. However, we like that this trade would make many in the marketplace uncomfortable. We were in that position last week. This is a time when volatility supply decreases, leaving more room for those willing to take on the risk.

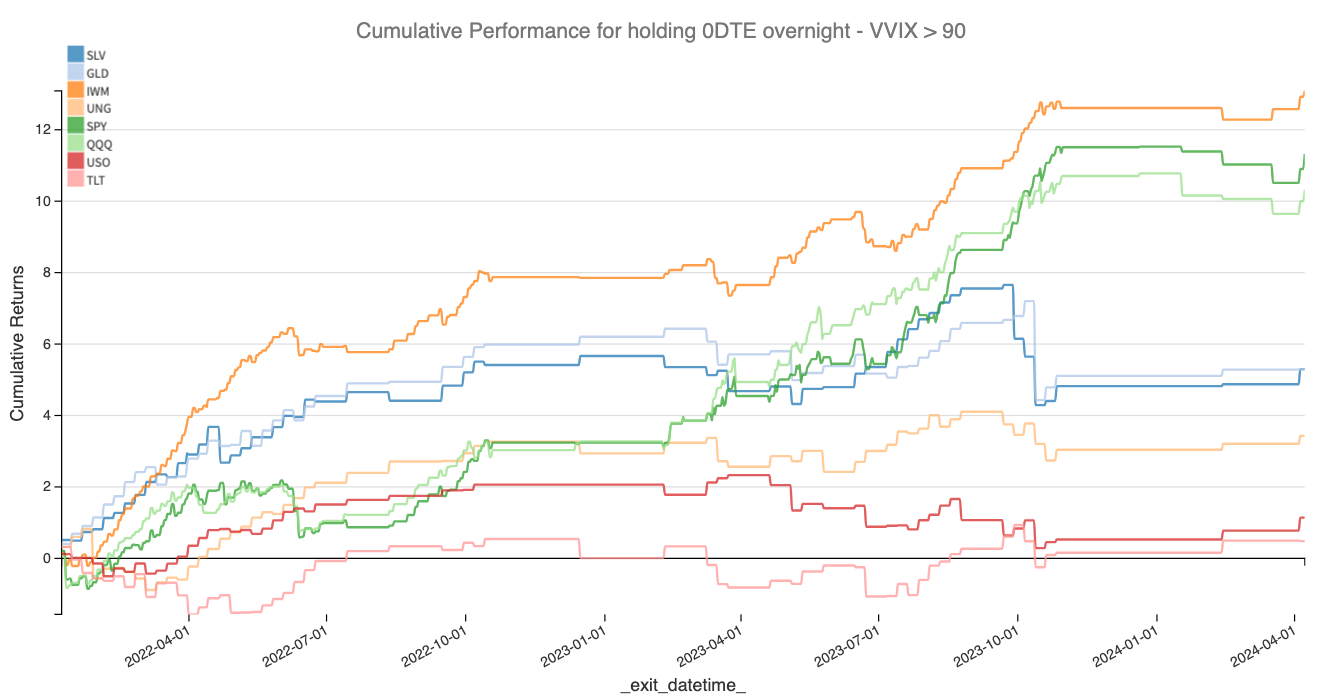

Is the result consistent over every asset class?

But does this hold for every asset class? As a reminder, we've primarily looked at eight tickers. What would the performance look like for each ticker?

There's a clear premium for IWM, SPY, QQQ, and a more moderate one for Gold and Silver. However, could it be because VVIX is a great risk measure for equities but a little less effective for other asset classes?

What if we could examine a close equivalent of VVIX for each asset class? Would we see similar performance to what we observed in equities?

Stay tuned, and join us next week for the answer.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.