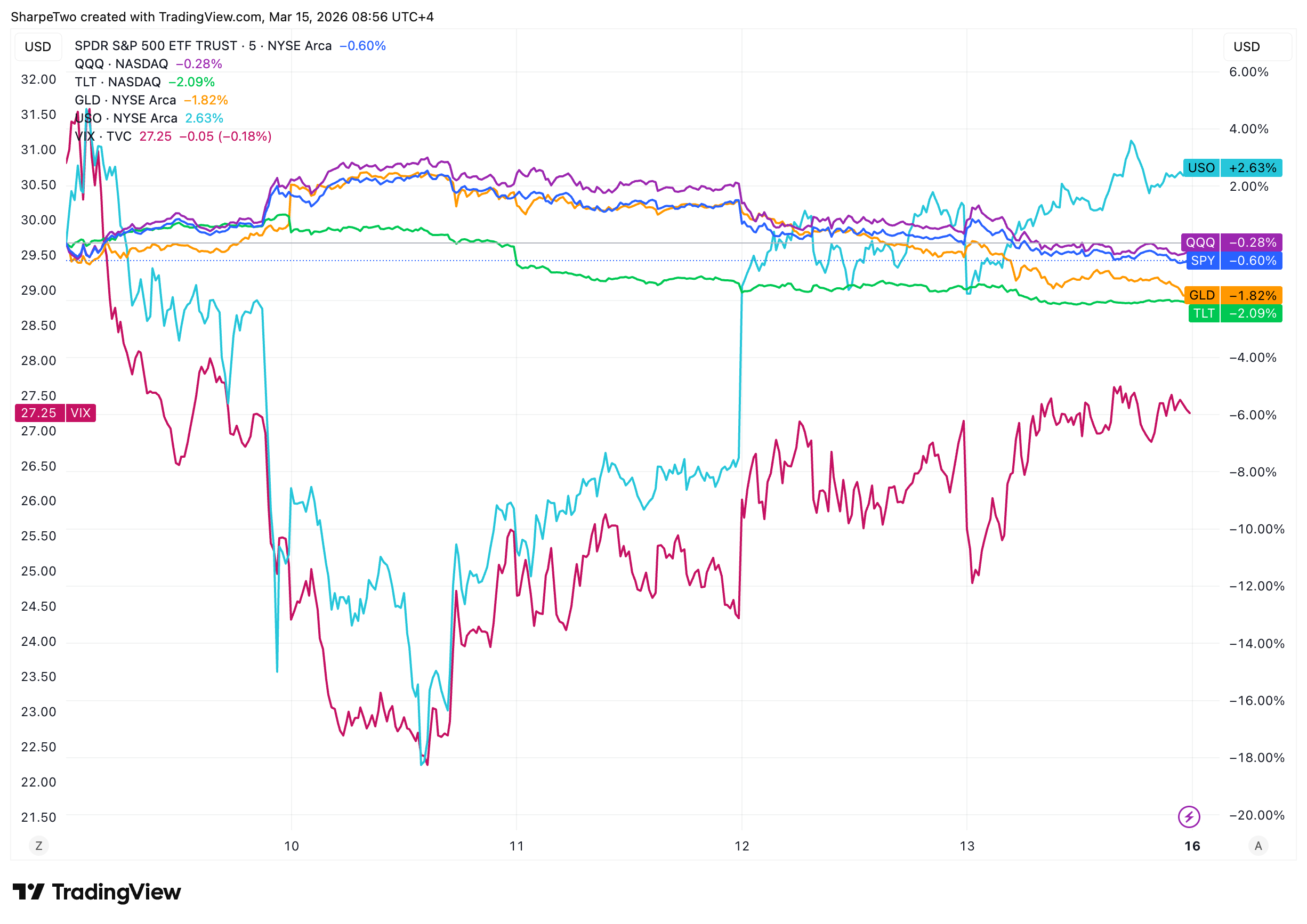

Equity markets finished the week down again as the mood darkens with the prospect of a longer war in Iran: the S&P 500 lost a little more than half a percent while the Nasdaq was pretty much flat. The VIX didn’t finish at 29 like last week, but the close at the 27 handle tells you everything you need to know: the uncertainty is high and after a week of reversal, we are left with many more questions and only fewer answers.

First of all, if you’ve enjoyed the 30% down day in silver at the end of January, you surely have enjoyed very much the 50% reversal from the high in oil. Let’s rewind: in the wake of an unresolved situation regarding the war and the nomination of Mojtaba Khamenei as the next Supreme Leader, oil went ballistic overnight on Sunday and was printing close to $120 a barrel, a +25% move from the close on Friday. This was enough to send some jitters down the spine of many politicians worldwide, and particularly the G7 countries, which quickly announced they would gather to release strategic reserve, or about 300 to 400 million barrels.

To put this in perspective, the world consumes roughly 100 million barrels of oil every day. A release of 300 to 400 million barrels amounts to three to four days of global consumption, and would be the largest coordinated release in history, more than double the 2022 response to the Ukraine war. Before that, the 2011 Libya intervention prompted a 60 million barrel release from the IEA. In short, we are in uncharted territory for the strategic reserves, and the fact that it took this much to stabilize oil around $100 should tell you everything about the severity of the disruption.

At that point, we thought the worst may have been avoided and if diplomacy can do its trick, one of the most serious geopolitical crises of the 21st century would have been aborted. Except diplomacy isn’t doing its trick. Iran has insisted that in the wake of continued bombing of its territory, the Strait of Hormuz will remain closed and that it will continue attacking American interests in the region. To which the US and Israel only retaliated with more missiles and destruction.

When and how this is ending? Nobody knows. Hence VIX 27, hence oil at $100. And for the first time since we do market commentary, there are enough ingredients in place to defuse the situation, but there are equally enough to make things much worse in the space of a few days or weeks.

So in that context, the goal is still not to be a hero, unless of course, you know what will happen. VIX 27 is rare enough to be respected: volatility clusters and doesn’t dissipate overnight, unless you have a clear path to resolution. And a resolution, in this case, is not about releasing emergency reserves; it is about reopening the Strait of Hormuz, and if possible without military ships being involved.

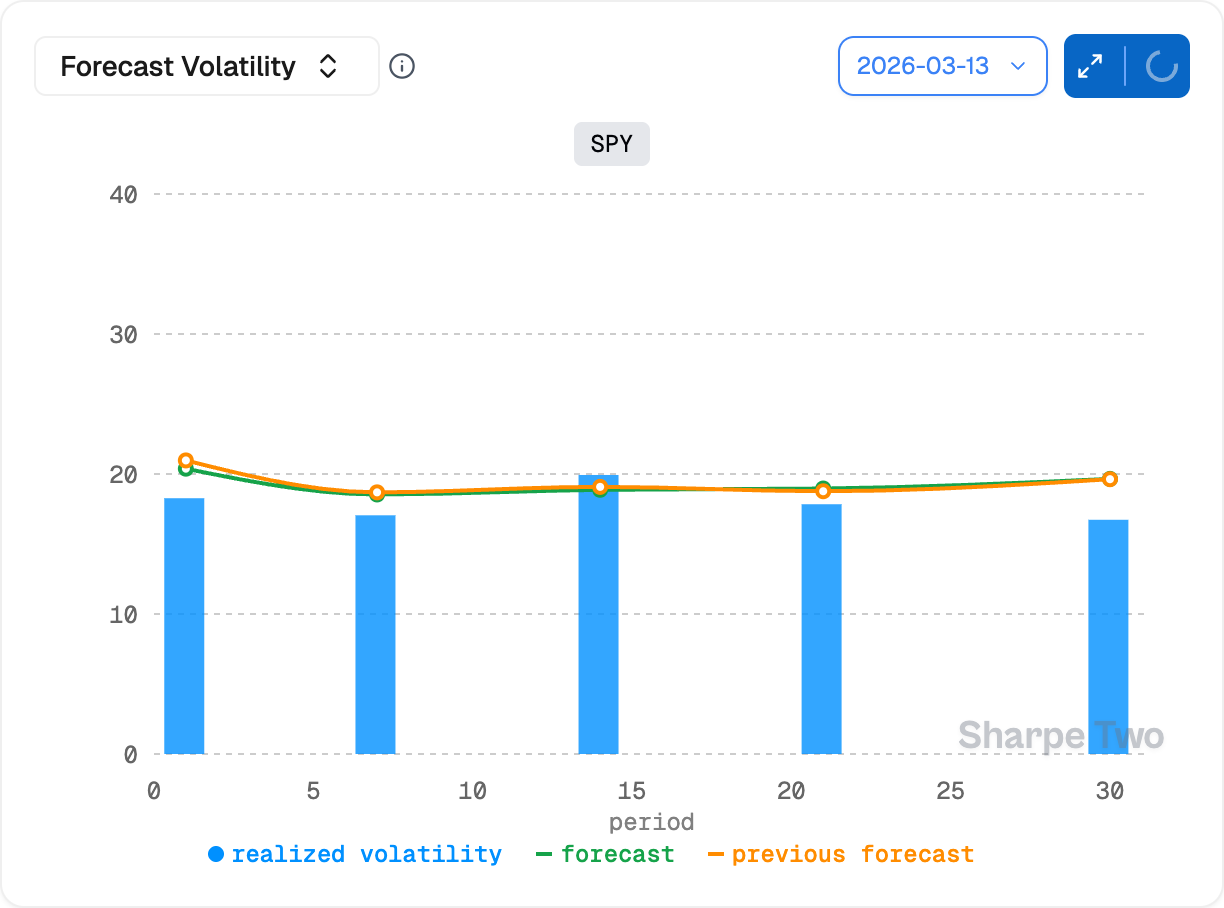

Realized volatility has been sitting right under 20% over the last 3 weeks and we expect it to be right there over the next month. In the current context 7 or 9 points of variance risk premium are still a lot and you should be able to get away with it. However, 17% realized volatility has nothing to do with 9%. The market is more likely to experience violent moves up or down, as the headlines follow one another and making sure that your delta stays in check is mandatory.

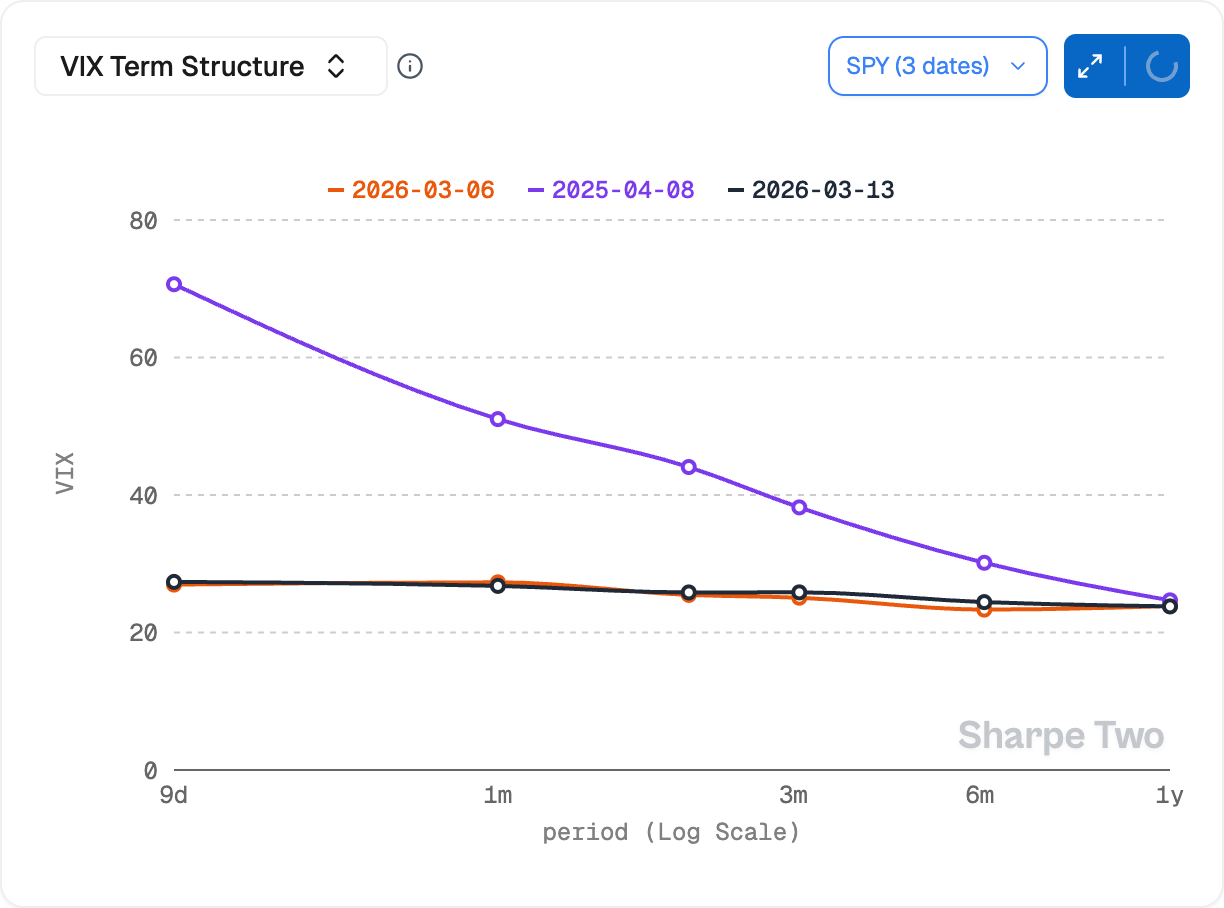

The term structure is pretty much identical to where we’ve left it a week ago. This means once more that if you have some trades in the April contract, you can still roll and recenter further out on the term structure at pretty much the same level of implied volatility. This is a great way to go find shelter while waiting for things to pass. We still think buying the back months to transform a short strangle into a calendar structure has value: better safe than sorry, because if an episode similar to April last year were to strike, the 3-month implied vol still has a lot of room to expand: yes, it can absolutely go to 40, almost overnight with very limited ability to do anything about it.

What about oil?

As one would expect we are in extreme stress territory, and let’s start with the obvious: you do not have to trade it. Extreme situations are appealing to many retail traders. And sure, if you know what you are doing, some amazing opportunities arise. The problem is that this is also the hill where fortunes are lost. If big commodities trading houses are securing lines of credit (Bloomberg reported this week that Trafigura, Vitol, and Gunvor have collectively lined up $7 billion in emergency facilities), you can imagine the carnage that this situation is currently provoking. Your job is to not be part of the casualties, and often that means staying away.

That said, because we know after three years of writing Sharpe Two that half our readership is sane, the other half has degenerative tendencies, what could be the trade? Well, you could see it that way: if things were going really crazy and USO reached 150+, it is unlikely that SPY would stay as well behaved as it has been. Therefore, one could consider selling extremely expensive USO calls at 3 months, and buy some expensive, but in comparison, cheap SPY puts at 3 months. If things calm down, you will most likely keep most of the premium in USO, and have financed a free tail in SPY in the process. And if things get really crazy, the call skew could protect you enough for the SPY tails to pay off.

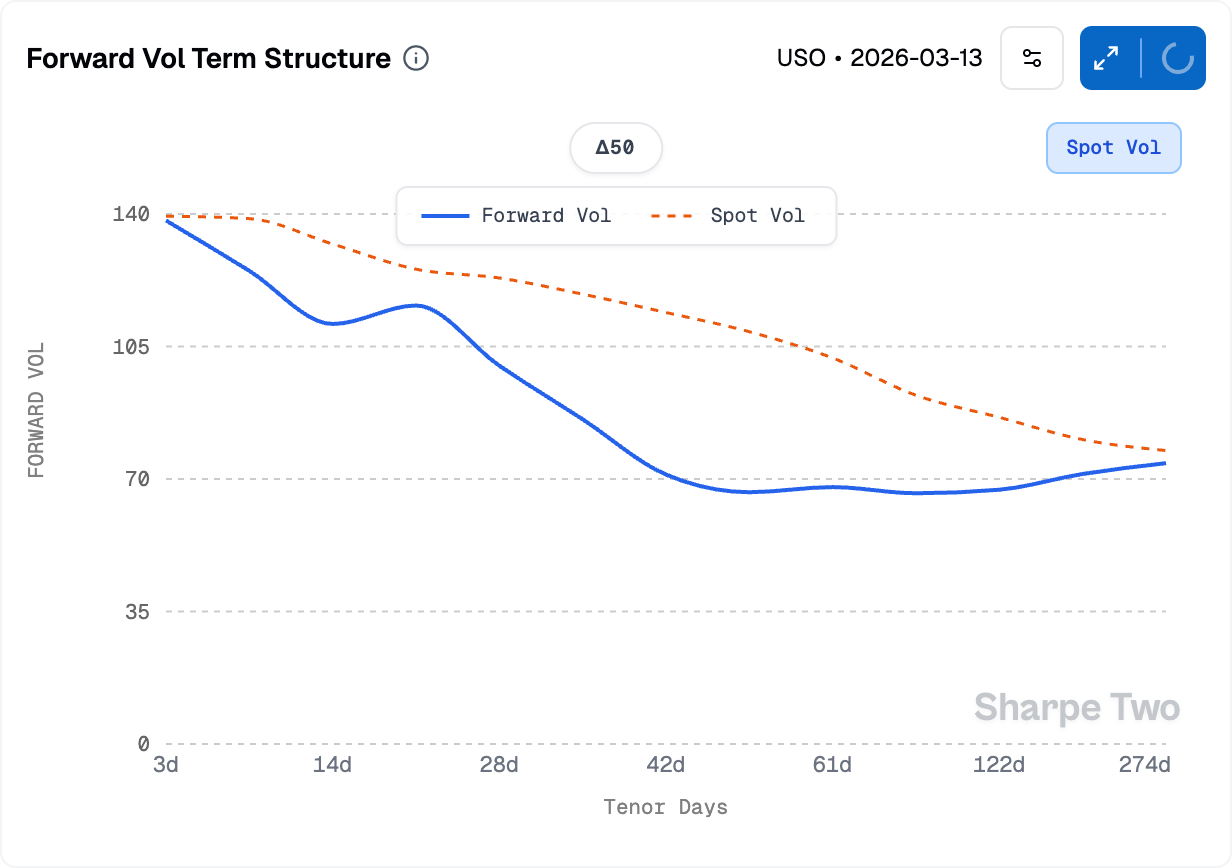

While things are still crazy and up in the air, the forward vol clearly points to event risk in the very short term for obvious reason, but then right during the expected visit of Trump in China. Coincidence? We do not think so: Panama and Hormuz in the same year will surely have a big impact on the discussions during the state visit scheduled for the end of the month. And after that? “smooth” sailing with forward implied volatility of “only” 70%. The goal, as always, is not to be a hero but to weather these bumps.

Good luck.

Sharpe Two is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

In other news

What is happening with regional banks and the credit crisis? To be perfectly honest, we have mostly ignored it this year, too busy being mesmerized by the commodities sector. But let’s recap: Blue Owl permanently closed redemption gates on its $1.6 billion fund in February, BlackRock gated withdrawals on its $26 billion private credit vehicle, and a top executive from Goldman Sachs was pointing out that the war in Iran was a convenient “distraction” from the real story: private credit is cracking.

Do we actually have something to fear here? At this stage, we will give the benefit of the doubt, but that is starting to be a lot of smoke. And the first set of answers may come from the Fed policy decision next week: it is hard to imagine Jay Powell announcing a rate cut in this context, but the statement should start to reveal how many cuts to expect this year, if any. And if rates stay higher for longer, what happens to all these credit organizations sitting on floating-rate leverage? We are often on the side of it being hard to fool the market twice on the same topic. But the smoke is getting thicker.

Thank you for staying with us until the end, as usual, here are two interesting reads from last week:

- Iranians rethink the price of regime change (FT) — Life continues in Iran despite the bombs. While the FT has a tendency to splurge on sensationalism when it comes to the “bombing” of Dubai, this piece brings you closer to what life actually looks like for ordinary people in Tehran right now. Introspective and, we hope, uplifting.

- And because we all need something uplifting after a week like this: a man with no biology degree used ChatGPT and AlphaFold to build his dog a custom cancer vaccine. Paul Conyngham, a machine learning consultant from Sydney, spent $3,000 on DNA sequencing and watched his rescue dog’s tumor shrink by more than half. No medical school, no lab, just publicly available AI tools and a man who refused to let his dog die. The implications for human medicine are hard to overstate. If that doesn’t put a smile on your face, nothing will.

That is it for us this week, we wish you a (peaceful) Fed week ahead, and as usual, happy trading.

Ksander