It is Central Bank week, with BOE, SNB, BOJ, and the Fed set to report on their latest monetary policy decisions. As a result, this week is expected to be pretty busy on the currency front. Although currencies are not an asset class we trade often, there could be some interesting opportunities to consider once all these events have passed. In particular, the implied volatility in the dollar index is currently elevated, expected ahead of such a week. Shorting the dollar index before these events would be very presumptuous—waiting for the announcements before capitalizing on the potential volatility crush is a much better approach.

In the meantime, it's best to use the sessions before Wednesday to trim some of the positions taken in the past few weeks and add some long volatility trades as a hedge. Today, we'll review some tickers in the bond complex:

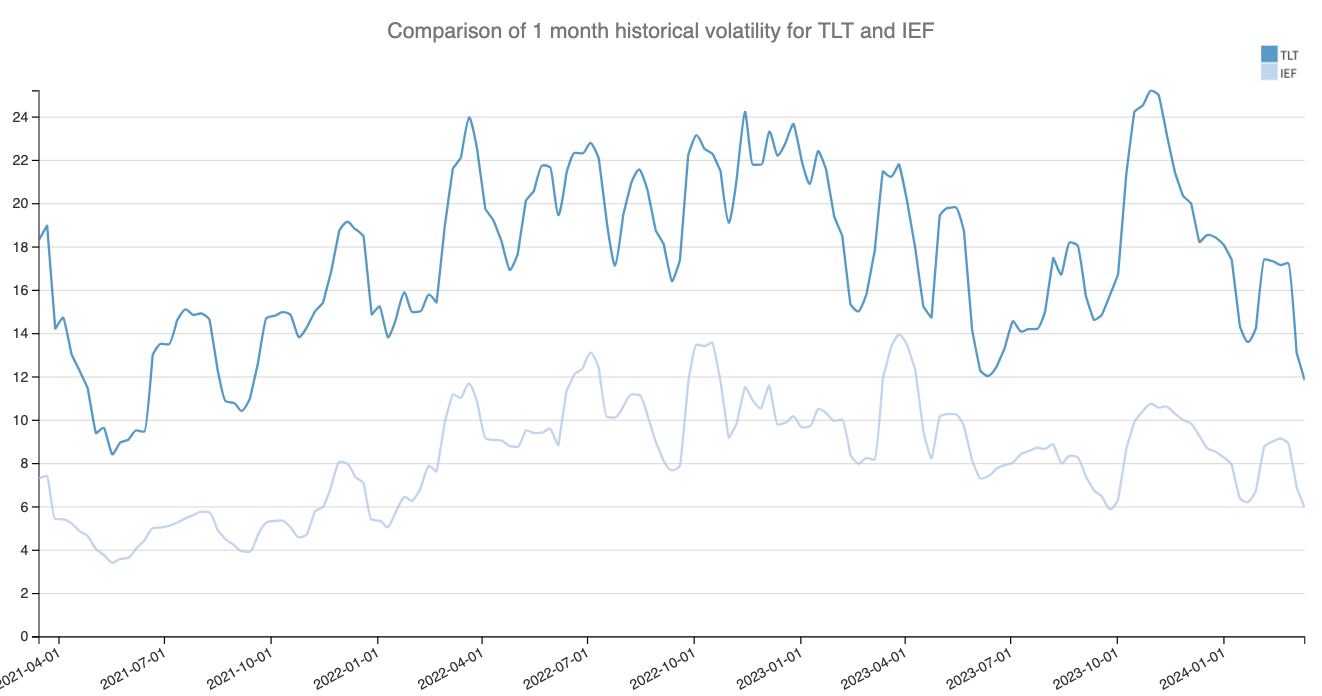

- TLT - the long end of the Treasury curve (20+ years)

- IEF - the intermediate-term of the Treasury curve (7-10 years)

Let's dive in.

The bond space has slowed down since the rally in Q4 2023

Since the turn of the year, the bond rally has stalled, and we are waiting for the anticipated rate cuts to materialize. That being said, the realized volatility in some of these bonds has significantly decreased from the highs observed during the hiking cycle and at the end of last year during the relief rally.

The FOMC meeting on Wednesday is pretty much priced in—the rate is expected to remain unchanged. What matters, though, is the anticipation for the rest of the year, which could significantly impact bond prices. With that in mind, these expectations will likely be reflected in the options prices for these products.

Let's take a look.