Jackson Hole is finally underway, and all eyes are on Chairman Powell's upcoming speech tomorrow morning in the US. But for now?

The equities markets are slowly drifting upward. With the VIX sitting at 16, it’s hardly surprising, right? But the real burning question is: Has volatility truly gone for good? It's always challenging to be certain, but we don't think so. Some of the data on equity markets suggest that implied volatility might be a bit cheaper than what’s been realized recently.

We've been hesitant to short more corners of the market. Instead, today, we’re presenting a long opportunity in EFA, the ETF that tracks the performance of global developed markets outside the US.

Let’s dive in.

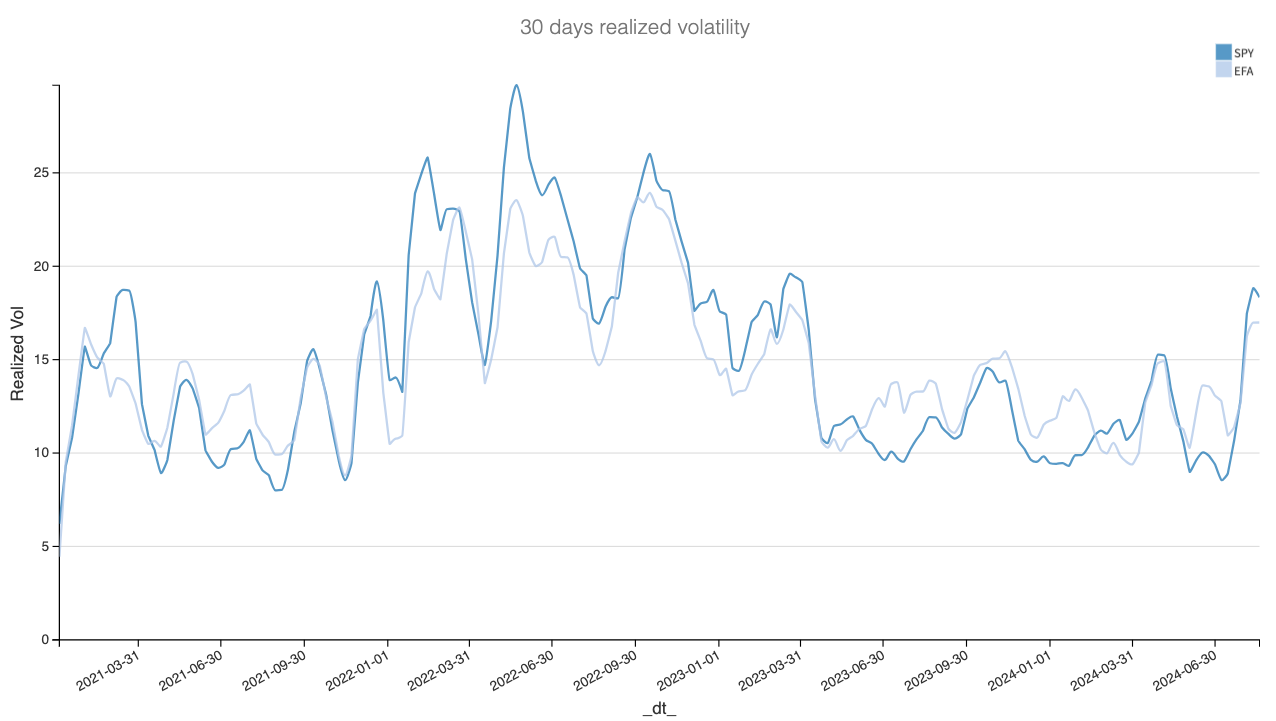

When the SP500 lost about 8%, EFA followed suit, dropping around 6%—just a few percentage points away from turning negative for the year. But then, the rebound came, propelling it back within inches of its high for the year.

Given that backdrop, it’s not too surprising that realized volatility is still elevated despite the relative calm of the past few days.

We’re still hovering around the highest levels observed in 2023 and navigating territory we hadn’t seen since 2022. So, caution is essential—we’re not entirely out of the woods yet.

Yet, in the wake of a VIX at 16, the options market is telling a completely different story.

Let’s take a closer look.

The data and the trade methodology

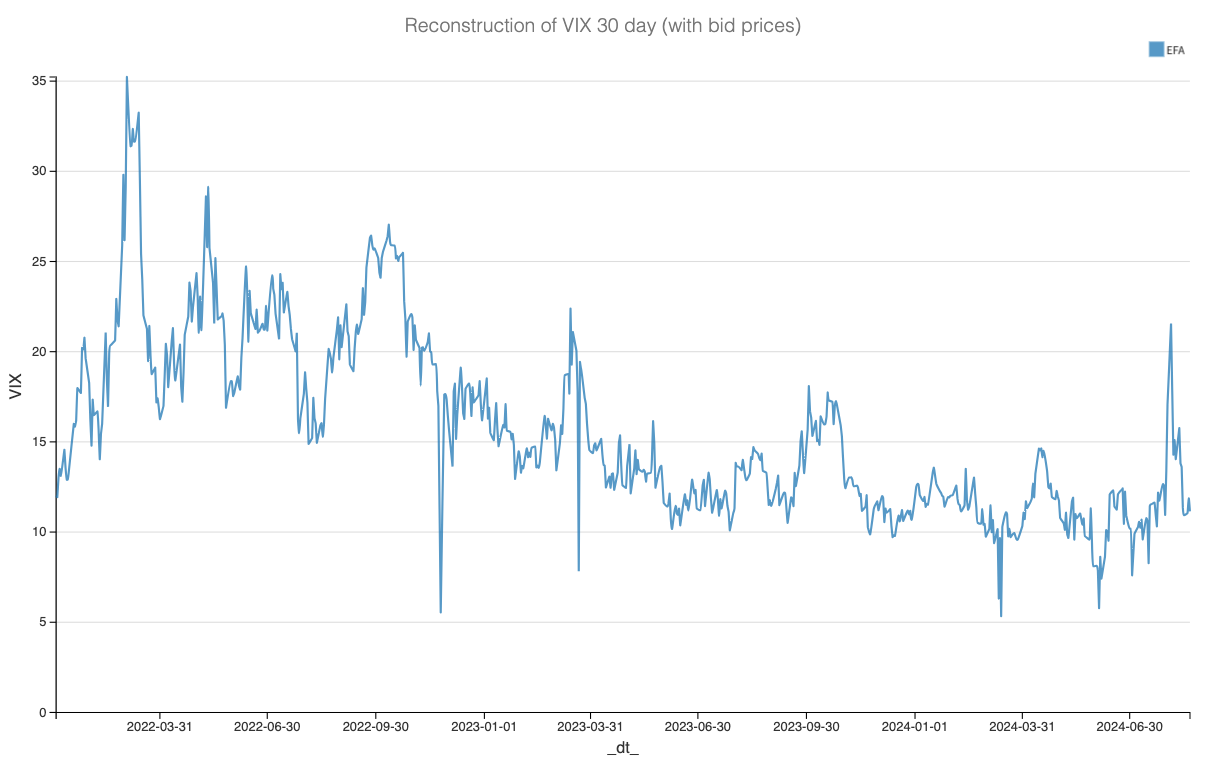

Much has been said about the fastest volatility crush on record, yet many in the market are still flabbergasted by its extent. Let's examine the implied volatility in EFA, measured using the VIX methodology.