The equity market has had its best days since Trump got elected, and the VIX is back at 16. Let’s see if realized volatility finally drops as we head into MLK weekend.

In the meantime, we’re diving into a trade opportunity in BOIL, the ETF that offers investors exposure to three times the performance of the natural gas market. We successfully sold some calls a couple of weeks ago as the skew tilted heavily toward the call side. Today, however, we’re shifting our focus back to the good old variance risk premium (VRP).

Let’s take a closer look.

That said, situations like this highlight where volatility traders can hold an advantage over directional trading: the key lies in assessing the current level of market risk and comparing it to what the options market implies without pandering if it will go up or down next.

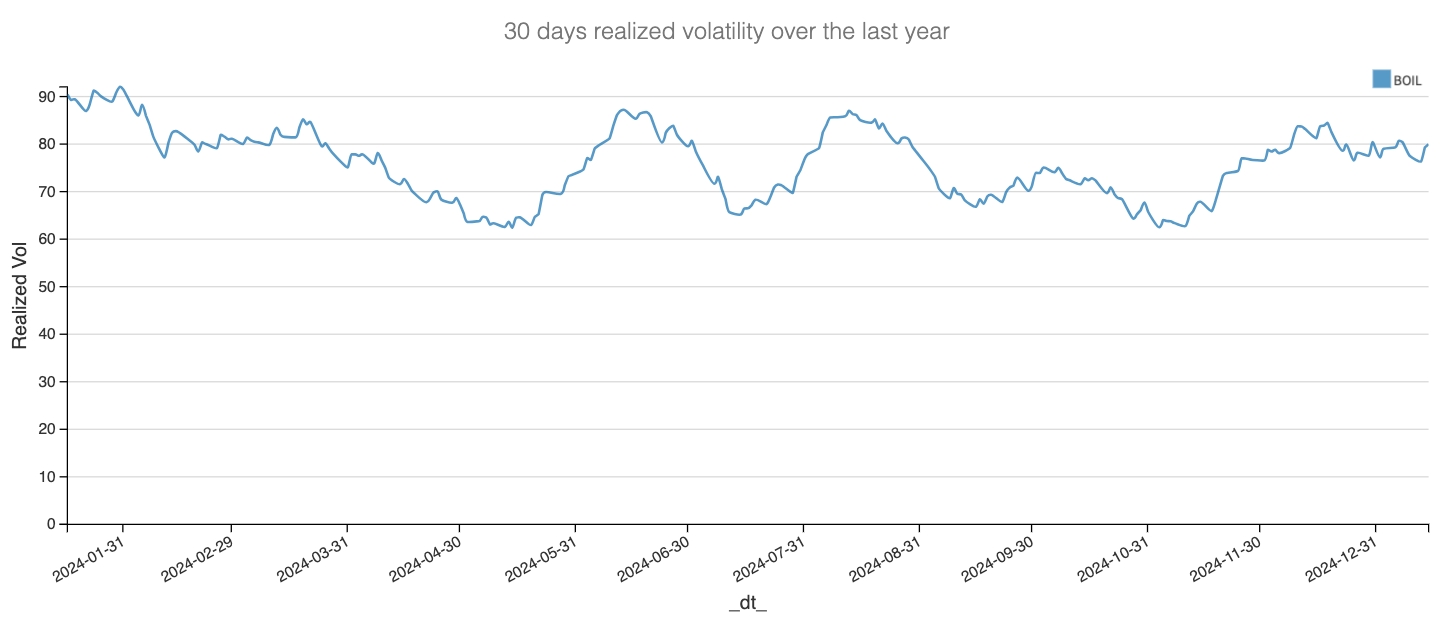

As expected, realized volatility has been climbing over the past few months but has stabilized around 80% throughout December, even as BOIL continued its upward march. While we don’t have a directional view on the asset, we can attempt to forecast realized volatility for the coming weeks.

At this stage, we anticipate realized volatility in BOIL to ease slightly, settling around 70%. While still high (compare it to the relatively calm 16% we’ve been seeing in SPY over the past month—spare a thought for those navigating natural gas markets), this expected decline gives us more confidence as we move into the next phase of analysis.

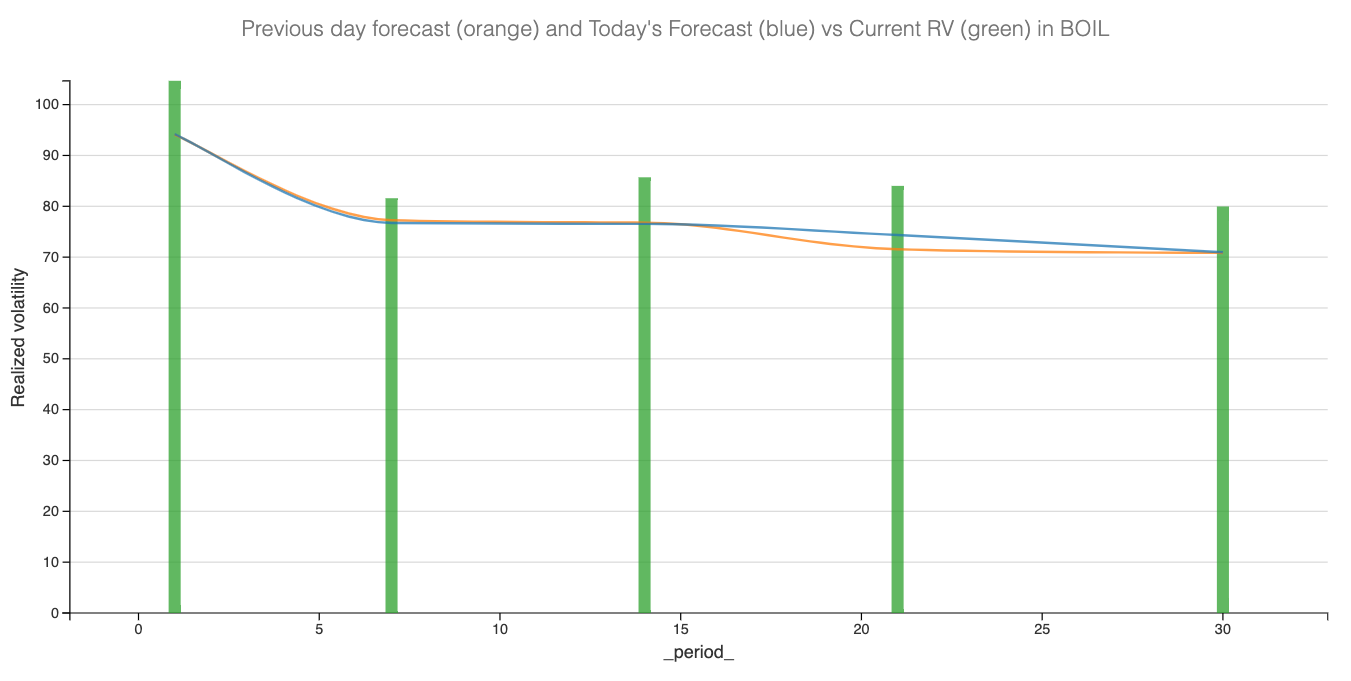

Let’s now examine how much additional premium is currently baked into the options market.