Yesterday's session in US equities was uneventful, and while we await the May FOMC meeting, there's a high chance that today will be fairly tame, too. But who knows? The markets have ways of doing things we mere mortals cannot comprehend.

Today, we'll take a look at something slightly different. We've been focusing on US indices lately, harvesting the high premiums from April as realized volatility comes down. Yet, the beauty of sectoral ETFs is that opportunities can arise anytime, anywhere.

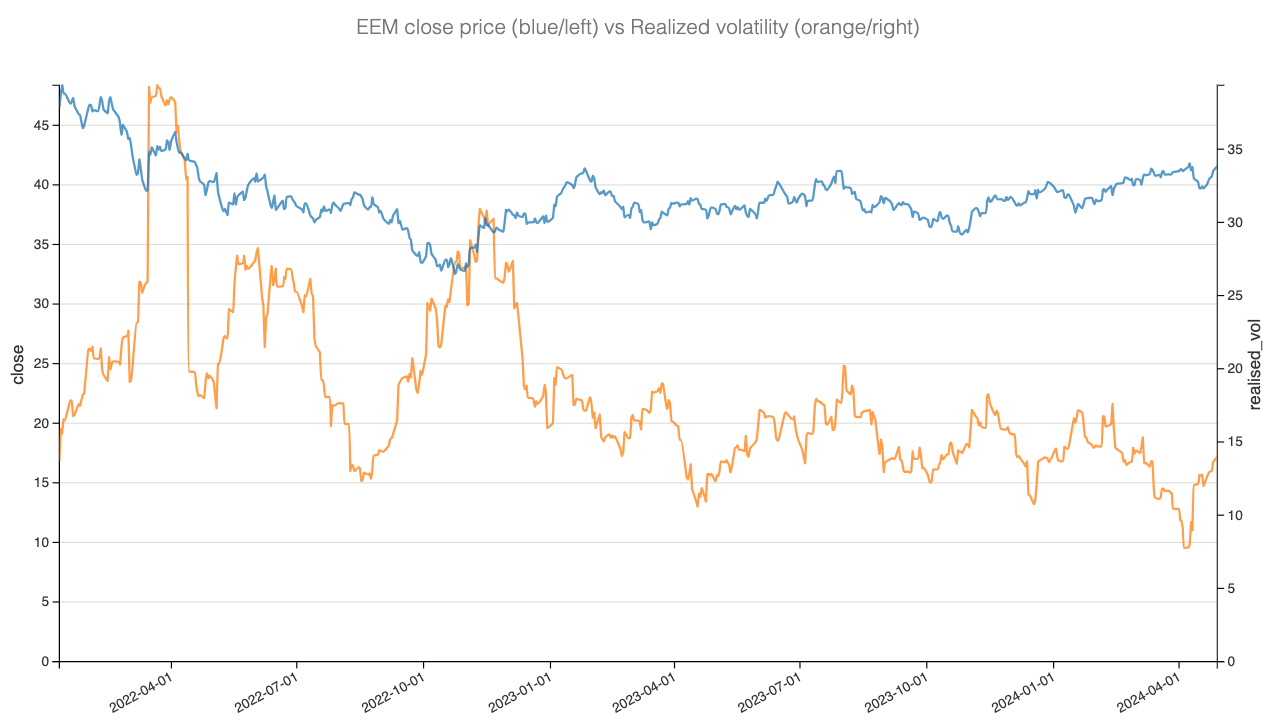

Today, we'll focus on EEM, the ETF that exposes investors to emerging markets.

Let's take a closer look.

source yahoo finance

Does that mean there's no risk involved? Not as much as in riskier asset classes, but the risk is not 0 either. This is reflected in its volatility profile.

With realized volatility below 15, we're far from the traditional risk profile of a risky asset.

In such a context, you wouldn't normally expect to see the options market attributing a huge risk premium to such an asset. Once again, where's the risk? You would need something major in the next two to three months to push it away from its current fair value, which seems to be around $40.

But once again, we're just Jon Snows and know nothing.

Let's quizz the options data and see what they say.

The data and the trade methodology

Let's start by examining the VRP using 30 DTE straddle prices. We'll compare them with an average of the 30-day elapsed move in the underlying.