The world can’t stop watching oil. Hormuz traffic is down 90%, two more tankers took projectiles overnight, and WTI opened above $94 after the IEA’s record 400-million-barrel reserve release barely made a dent. Reserves replenish supply but they can’t escort a tanker through a war zone. Caxton’s macro fund lost 7% last week, and these are people built for exactly this kind of environment.

But while crude dominates every headline, tech has been quietly building its own case for attention. AI spending keeps making the news for all the wrong reasons as investors have run out of patience for promises without profits, and the circular debt narrative from Q4 never really went away. It just got overshadowed by a crisis in the Persian Gulf.

Here’s the thing, though. If you pull back from the noise and look at what QQQ has actually been doing, the picture is more nuanced than the mood suggests. The Nasdaq 100 is down about 5% from its November highs, and the decline has been orderly, more a slow grind lower, not a crash. Realized volatility, while elevated, hasn’t gone anywhere near the levels you’d expect given the barrage of negative headlines.

QQQ sits at the intersection of genuine macro uncertainty and what might be a very expensive options market. Our short vol signal list picked it up as one of the highest-conviction names this week. When we dug into the data, the case for selling premium turned out to be more compelling than we initially expected.

Let’s have a look.

QQQ price action, October 2025 to March 2026. Source: TradingView

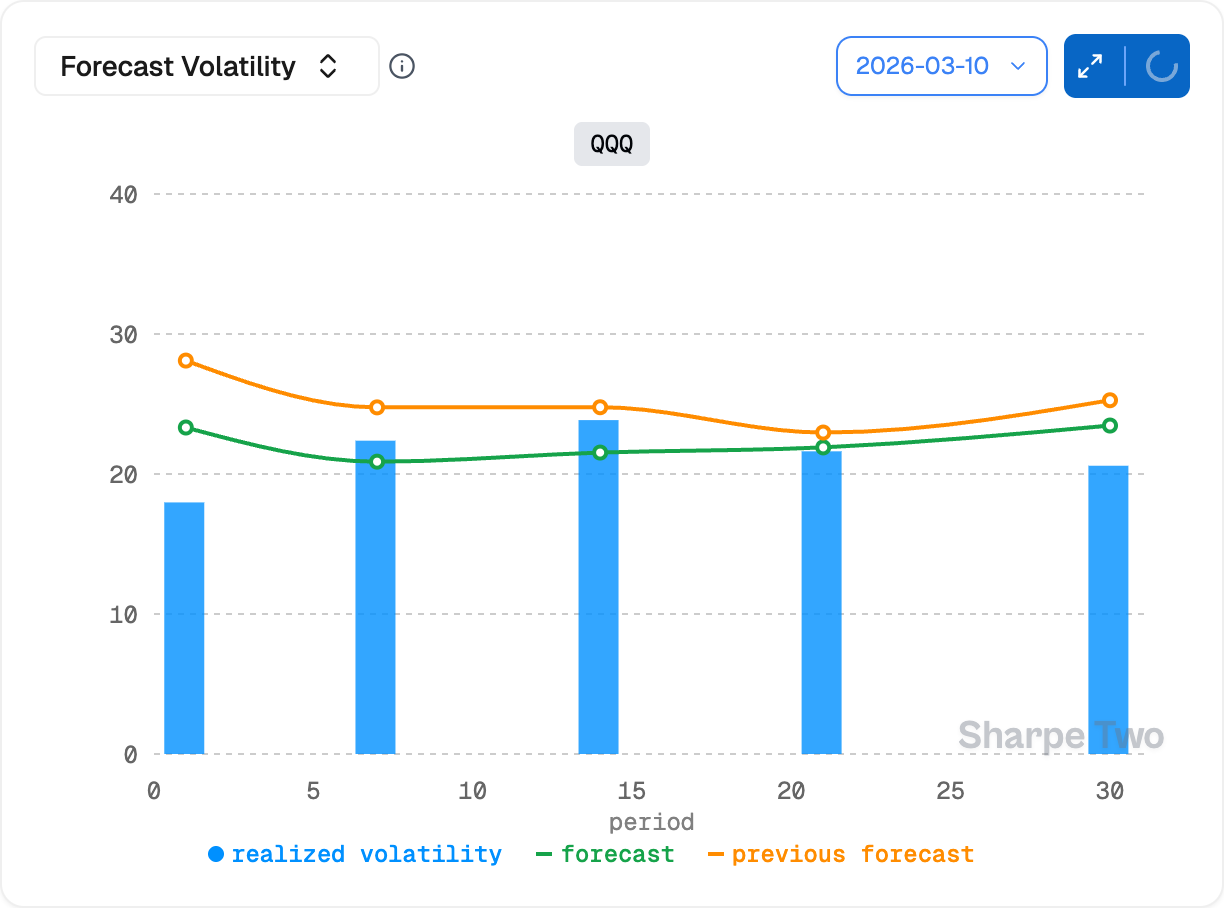

What’s worth paying attention to is how measured the actual price swings have been. Thirty-day realized volatility is sitting at about 21%, which sounds elevated until you put it into context. Compared to its own history, QQQ’s current RV sits between the 50th and 80th percentile of its vol cone, the median being around 17% and the 80th at 25%. Higher than normal? Sure. But this is far from distressed territory.

What caught our eye is the recent trajectory. In early March, realized vol spiked toward the upper end of the cone as a wave of selling hit the tech sector. But the spike was short-lived and within a week, RV started rolling over. The current 21% represents a market that got stressed briefly and is already decompressing. If you’ve been waiting for a moment where realized vol is elevated enough to matter but not enough to signal genuine trouble, this is what that looks like.

Our realized volatility forecast for the next 30 days expects a climb from the current 21% to about 23%. That’s a meaningful uptick but more of a grinding increase than a sharp move higher, consistent with the choppiness we’ve been seeing, not a precursor to something worse.

With that in mind, let’s see how the options market has reacted and where the best opportunities lie.