Yesterday was another significant day to the downside as the volatility spike expanded: we closed above 18 and even tested 19 in the overnight session. After months of ultra-low volatility, our regime classifies the current period as neutral. The holidays are over, and everyone is back on deck.

Another notable statistic is that the SP500 finally experienced a drawdown of more than 2% after 329 days. Is this the start of something major? You know us; we refrain from making big directional bets. However, panic has taken over social media after months of an easy upward trend and PnL screenshots galore. While some participants were caught off guard by the rapid move down, many seem to have forgotten what a neutral volatility regime feels like. They may very well be overpaying for insurance these days.

In this context, today, we propose a trade in SSO: nothing related to a cyber security ETF and the Single Sign-On protocol for the geekiest of us —but the leveraged ETF on the SP500.

Spooky, spooky. Let’s take a look.

The relationship between the two has always been extremely strong, especially since 2020. However, when you start to see some abnormal returns for the SP500, the ETF may not perfectly replicate what is expected: it slightly underperforms on the way up and down. Yesterday was another good example: the ETF lost 4.69% while the SP500 was down 2.29%. It's close enough, but not exact.

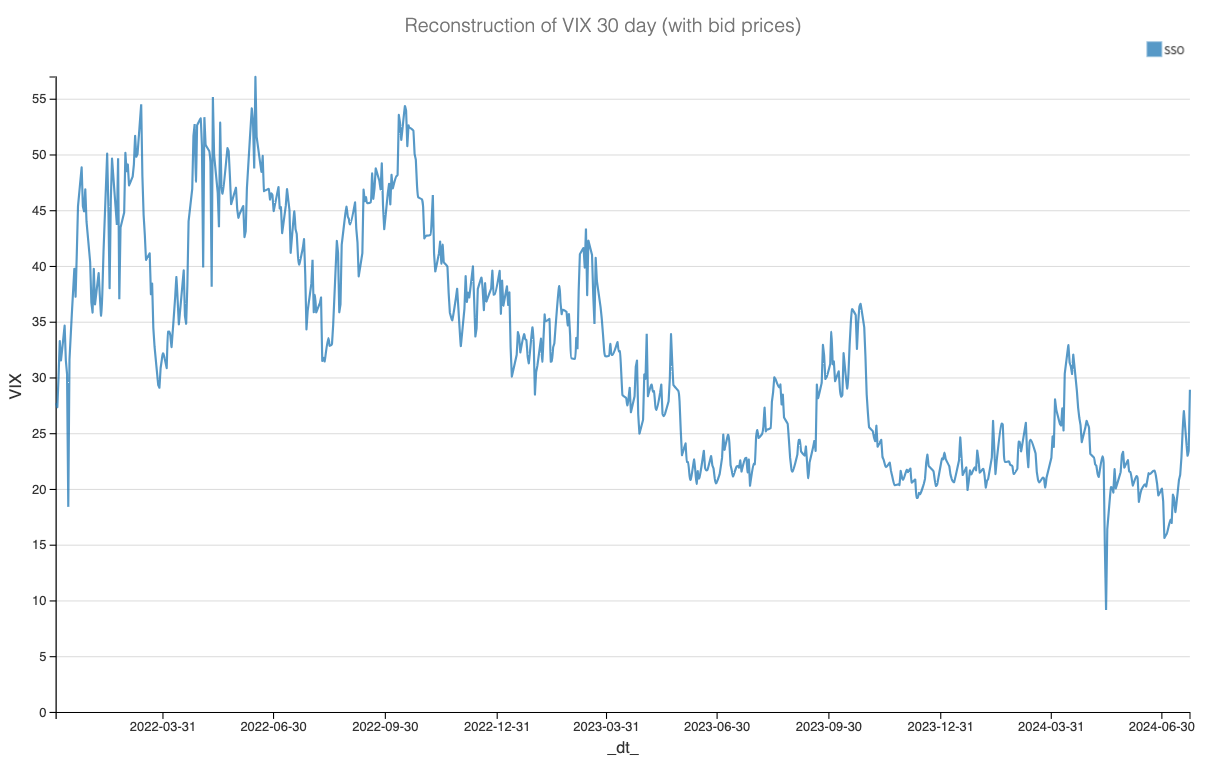

This additional uncertainty is crucial when trading leveraged ETFs: traders are aware of it and tend to add a cushion to factor in some "ETF operational issues." But before diving into the options data, let’s look at the realized volatility in SSO.

When you put it in perspective like this, you can see that despite a slight move up, the realized volatility in SSO is still at its lowest observed over the past two years. Whether things will keep accelerating and bring it back to 35 is an interesting debate: next week will be very busy, but after that, what? So, is there a possibility that option prices may have overreacted to the recent move down? Let’s find out.

The data and the trade methodology

Let’s state something clearly: while shorting volatility, we are not saying nothing will ever happen or that the bulk of the move is behind us and we can go back to normal. We are simply saying that things may not be moving as much as what is currently reflected in the options prices.