Once again, the world hasn’t ended—yet.

We're keeping an eye on the market’s response to the upcoming GDP data release. However, NVDA, after initially dropping as much as 10% following its earnings announcement last night, has recouped most of those losses and is now only down by a modest 2%. For traders accustomed to NVDA's typical realized volatility of around 70% in August, this is just another day at the office.

And since we've made it through this tumultuous August relatively unscathed—despite a swift and intense selloff and the VIX spiking above 60—we're considering a trade that might still seem daunting to many in the marketplace. Today, we're looking at a short volatility position in VXX.

Let’s dive in.

No all-time high? That is a first in 2024.

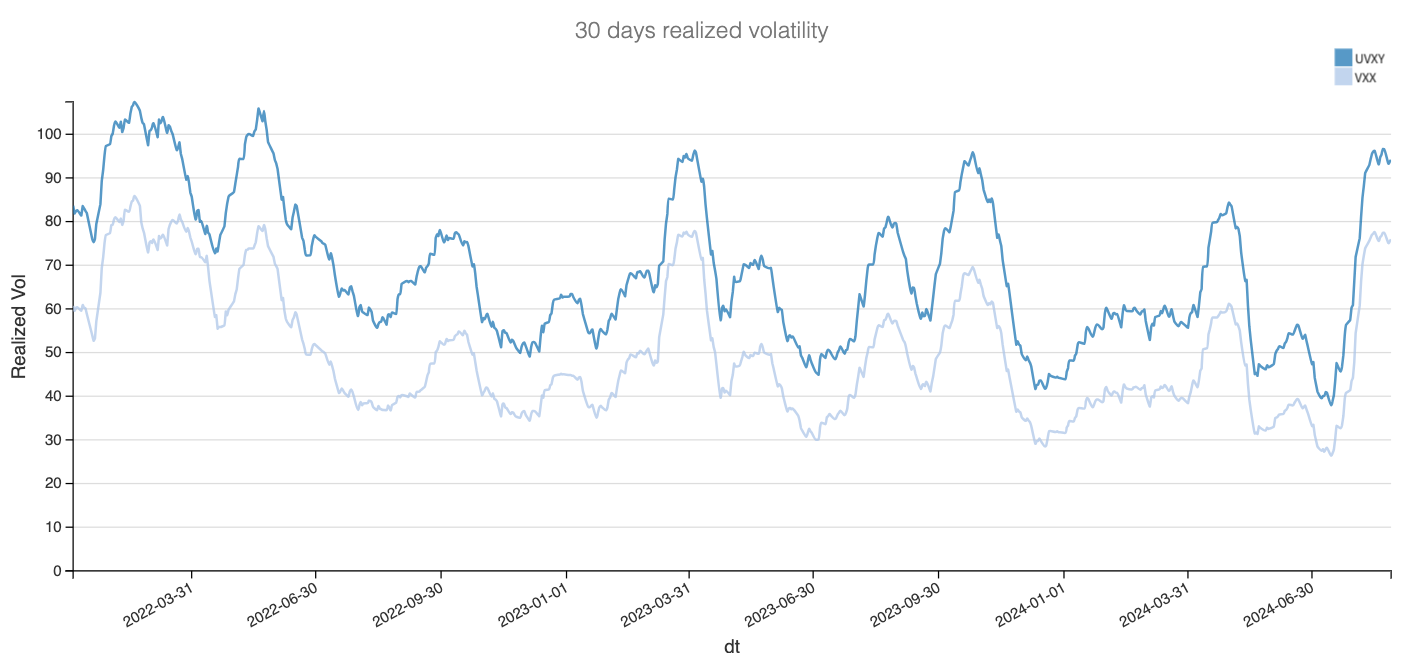

Despite the promise of a new rate cut cycle, some better economic data than late July, and a generally solid earnings season, the markets have yet to set new all-time highs. True, a 10% rebound over roughly two weeks was nothing short of remarkable, but still—the VIX didn't manage to return to its lowest readings of the year and, more notably, realized volatility in related products remains stubbornly high.

We may be peaking, and the 30-day realized volatility will descend from here. Realized volatility typically reverts to its long-term average, and with a less congested calendar ahead—and the world evidently not ending—it doesn’t seem too far-fetched to anticipate a downturn.

However, August's recent turmoil may still be fresh in the minds of options traders, prompting them to demand substantial premiums for shorting volatility in these products. Let’s dive into the data to see what it reveals.

The data and the trade methodology

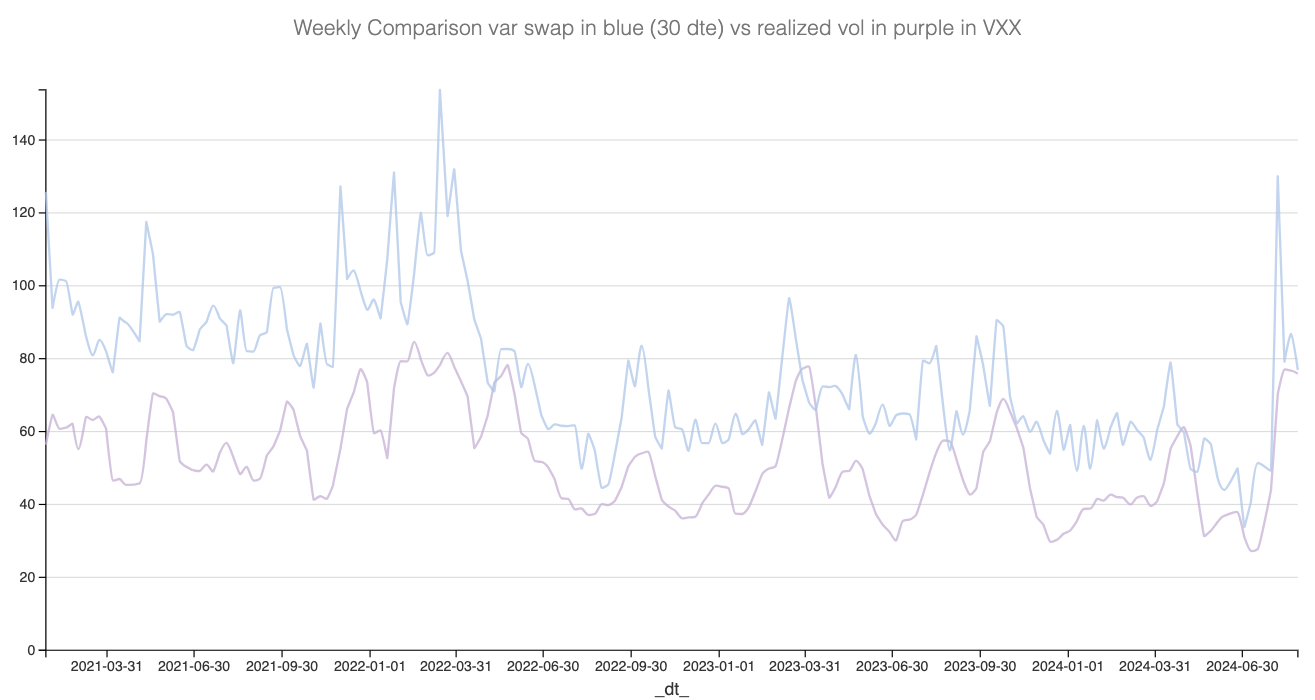

Let’s begin by juxtaposing the realized volatility we've discussed with the level of implied volatility, utilizing the price of 30-day-to-expire options in VXX for our analysis.