We ended last week with the lowest VIX readings in over four years. Despite significant developments in the Middle East over the weekend—including the death of the Iranian president in a helicopter crash and a potential warrant from the International Court of Justice against four Israeli leaders, including Netanyahu, for war crimes—the futures opened green and unfazed.

At VIX 12, the VRP is harder to find but hasn’t disappeared entirely. There are still corners of the marketplace where it is likely present, even at these super-low volatility levels—specifically, the volatility of volatility.

Today, we explore an opportunity in UVXY, an ETP tracking the VIX's performance. Yes, this trade can be intimidating—what if something goes wrong and the VIX skyrockets? Remember, your role is to manage the risk no one else wants to take.

In such a case, we would get hurt, but not more or less than any other volatility trade, as long as we treat it as just another position with no extra leverage.

Let’s take a closer look.

It’s getting hard to ignore these low VIX readings.

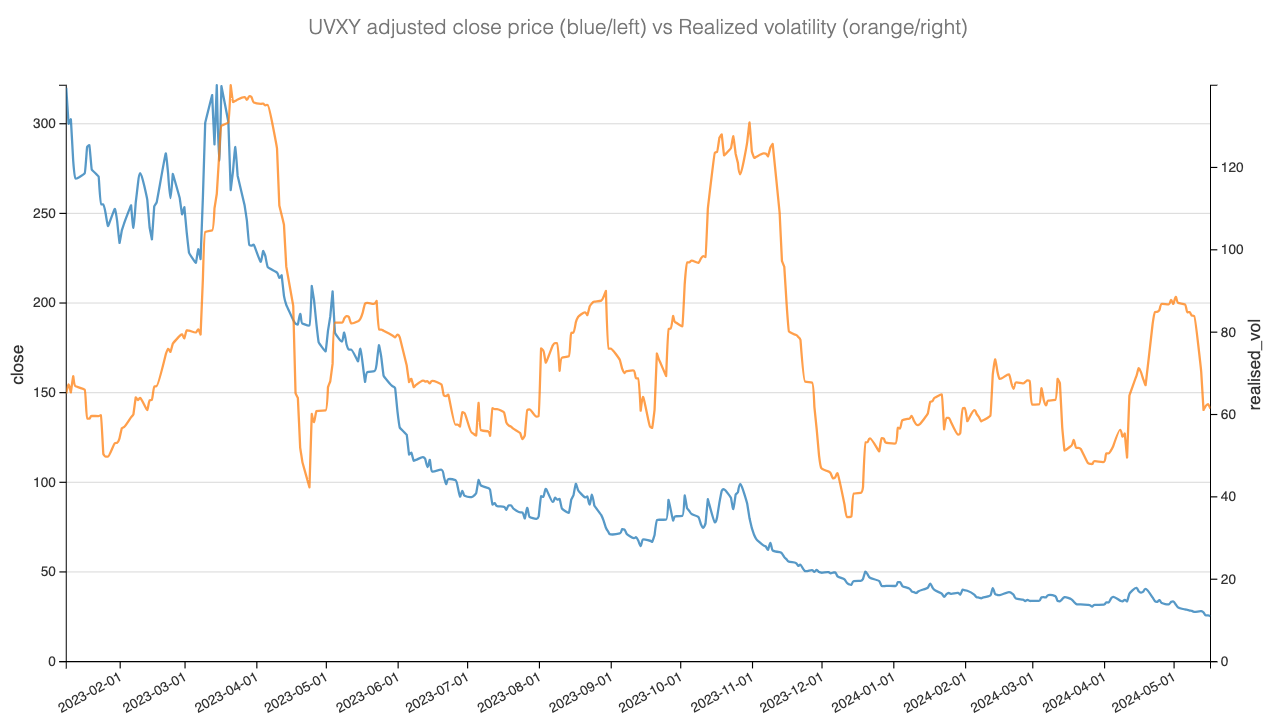

With the VIX this low, volatility products like VXX and UVXY have been consistently pulled down by gravity, constantly reaching new lows. About a month ago, UVXY underwent a reverse split (1:5 ratio), moving from about 7 to 35, making it easier for managers and interested parties to trade it.

Considering the natural contango in VIX futures, UVXY tends to drift downward, shortening this product's natural position. This is a good strategy; ensure your sizing is in check, as something significant will inevitably happen at some point.

A less common approach is to examine the volatility of the product itself.

We can gauge the product's realized volatility over the last 30 days using the adjusted close price. As expected, these are some of the lowest readings of the year. However, due to the product's inherent risk perception, the variance risk premium is unlikely to be too compressed.

Let’s dive into the data.