We woke up this morning to a steady overnight session. The Middle East front remained quiet, and China delivered relatively good news, with GDP topping expectations at 5.3%.

Is that enough to trigger a relief rally? At Sharpe Two, we don't take a stance on directional trades, but we'll keep an eye on the VIX, which closed above 19 yesterday.

Will that deter us from taking a short volatility trade? Absolutely not. In fact, unlike yesterday, we will take the scary trade with a scary name. Today, we're focusing on the infamous VXX, the ETP that provides exposure to VIX performance.

Spooky, spooky? Remember, this is ultimately why short-sellers are compensated: for providing insurance contracts when the marketplace is terrified and becomes price-insensitive in its quest for hedging.

Let's take a closer look.

VXX converges towards 0 overtime.

The adjusted VXX price over the past two years perfectly illustrates this well-known and documented effect. However, our focus here is not on taking a directional bet on VXX but rather on its volatility.

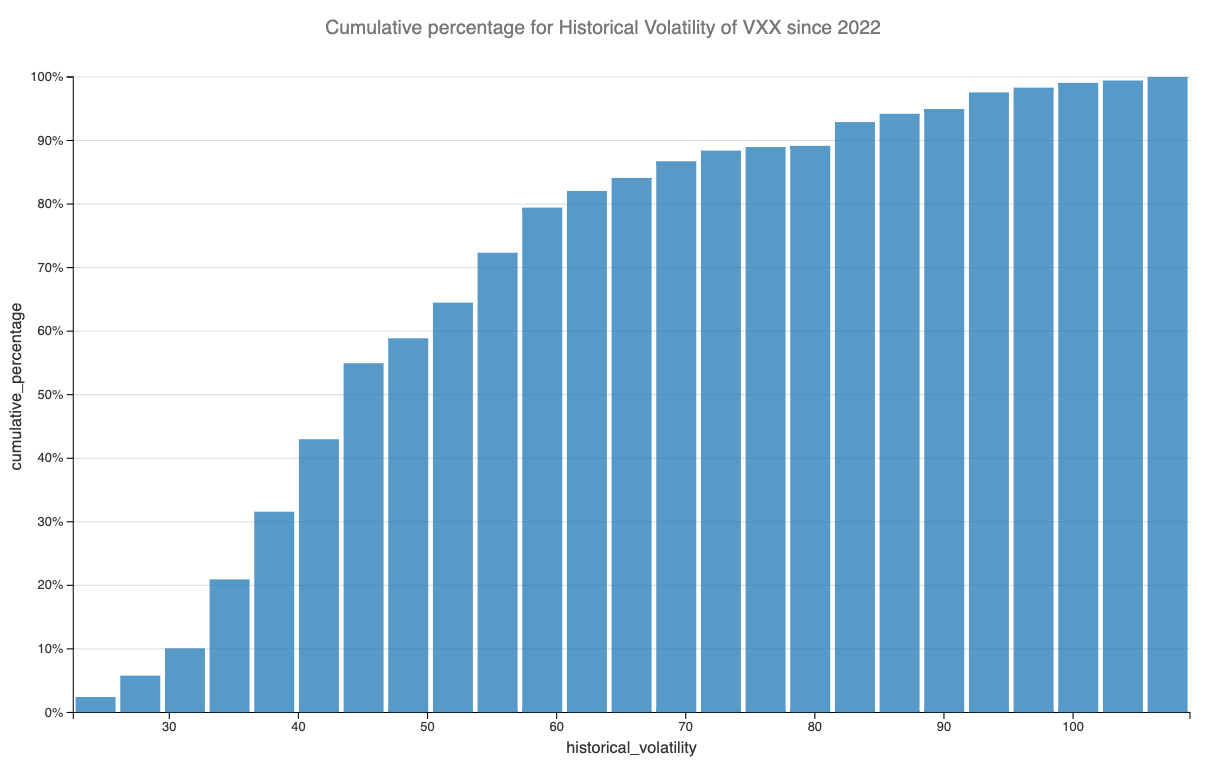

The realized volatility is currently in the high 40s, approximately in the 50th percentile of values observed over the past two years.

It can go much higher, especially if the newswire deteriorates over the next few sessions. However, due to the asset's scary nature, the prices of straddles in VXX have likely jumped even more than usual, overstating the risk observed in the underlying.

Let's dive into the data.

The data and the trade methodology

If you think about it, straddles in VXX are somewhat akin to taking a position in VVIX, the volatility of the VIX.

Let's examine the reconstruction of the VIX index for VXX using 30-day options.