A list of “good stocks” is not an edge when it comes down to options trading. It feels practical as you focus on a few names and sell puts or calls every week. Hopefully you make a few profits and soon after you system becomes that “little strategy that works for you”.

But that’s not a system or a strategy. It is hope in disguise.

That’s the part most retail traders miss. They build emotional comfort around a handful of tickers: TSLA, SOFI, PLUG, whatever is trending this month. The repetition feels familiar and safe. And that’s where it becomes dangerous, because loyalty or familiarity doesn’t move odds in your favor.

Premiums aren’t generous because your stock is “good.” They’re generous because someone, somewhere, is willing to pay up for protection and the price of that protection shifts daily, and with it, your odds of success.

The ticker or the DTE doesn’t decide your odds. The volatility surface does, and the volatility surface is nothing else than supply and demand and with the distortion that comes with it.

Most traders never connect those dots. They see premiums and miss the probability aspect of trading.

In this article we will see why retail keeps chasing “good stocks,” what professional desks actually do instead, and how understanding volatility — not tickers — is what separates consistency from coincidence.

Why Retail Traders Keep Searching for “Good Stocks for Premiums” (and Why It Never Works Long Term)

If retail traders keep asking “for a list of good stocks” online, it’s not stupidity though. What they really want is repeatability or something that feels predictable enough to trust.

That’s why the wheel and covered calls get labeled as “income strategies.” The appeal is structure and simplicity. And ultimately, retail wants what every trading floor wants: to automate decisions and spend energy where it matters most; risk and sizing, context and regime analysis. In the end, while they reduce randomness, they want to increase control.

The difference is how they do it. Institutional trading desks automate data analysis and ML pipelines. Retail automates comfort and familiarity: “I made money in this stock, I hope it will work again.”

That’s why they keep coming back to the same tickers, the same playbook. and why every week social media are filled with posts about how_“I found a little strategy that works for me.”_ And right after, the same follow-up: “Which tickers? Which DTE?”

It might work for a while — long enough to feel like knowing the stock gives you an edge. But does it? Not really. Knowing your stock doesn’t change your odds of success: knowing the dislocation of the volatility surface for a ticker will follow does.

How Professional Traders Use Volatility Data — Not Stock Picks — to Find Edge

Institutional desks figured that out a long time ago. They didn’t build habits; they built scanners.

Professionals want the same thing as everyone else; repeatable, systematic setups that make money over time. But they define “repeatable” very differently.

They don’t start with a ticker. They start with conditions.

The most basic one is the volatility risk premium — the gap between what the market expects to happen (implied volatility) and what actually does happen (realized volatility). When implied sits above realized, option sellers earn carry. When realized catches up or overshoots, it would have been a great time to own optionality.

That’s the simplest form of edge in volatility: selling insurance when the market overprices risk, buying it when the market underprices it. The game is knowing when each is true.

Quant desks have invested huge amount of money to build advanced data pipeline and that is why they rely on quants, software engineering talent. But the result give them an edge: they know when VRP is wide on SPX, when it’s compressed on QQQ or when sector ETFs start to decouple.

They monitor how much extra premium the market is charging for downside protection (skew), how steep the term structure is, how front-month volatility trades versus the back. And that is how they make money: they end up more often than not, at the right place are the right time. Not because they know a ticker in and out, but because they have the analytics telling them what to sell or what to buy.

Wondering if you should have sold options after the 2025/10/10 selloff? The answer was in the surface.

Retail never sees that because they’re not looking into analytics, not because they are lazy but often by lack of knowledge (thanks to all the youtube videos focusing on the wrong things), or simply because they do not have the time for this. And they end up focusing on names, instead of the analytics.

That’s the real difference. Pros aren’t necessarily smarter but they work for institutions that have invested millions to replace “familiarity” with math.

The Myth of the “Premium Stock” — Why High Option Premiums Often Mean Higher Risk

The lesson for retail is simple: stop asking which stock. Start asking where volatility is mispriced. Be ticker-agnostic. Focus on conditions where the odds quietly tilt your way. And if you have to, invest in tools showing you where the conditions are in your favor.

When people talk about a “good stock for premiums,” what they really mean is a stock with big numbers next to the options chain. Fat dollar premiums, tight bid-ask and ideally high number in the open interest. Feels like easy money, right?

But those “juicy” premiums are not a sign of edge, they are often compensation for idiosyncratic risk. Earnings or ex-dividends gaps. FDA announcements. CEO tweets. Sector rotations. All the random stuff that can send a single name flying while your short put disintegrates.

A big premium doesn’t mean good odds of profit in the end; it means the market sees landmines you decide to ignore and happily rent your account to someone trying to hedge the risk. Before accepting the trade, you should have an idea of if you are correctly compensated for the risk, the risk being measure through realized volatility.

Stocks are beast of their own anyway and at Sharpe Two we prefer ETFs when we sell volatility. The index smooths out single-name noise. SPY, QQQ, IWM, you can still harvest volatility risk premium there, but without worrying about a biotech headline blowing up your PnL.

ETFs also make the surface readable. The skew, term structure, and forward vols behave in line with macro regimes — interest rates, liquidity, positioning. You can actually see when volatility is overpriced or cheap.

When implied volatility trades above what the market actually realizes, short vol works. When realized breaks above implied, it doesn’t. Everything else — the ticker, the DTE, the strategy name — is just packaging sold by people really good at marketing, maybe a little less at trading.

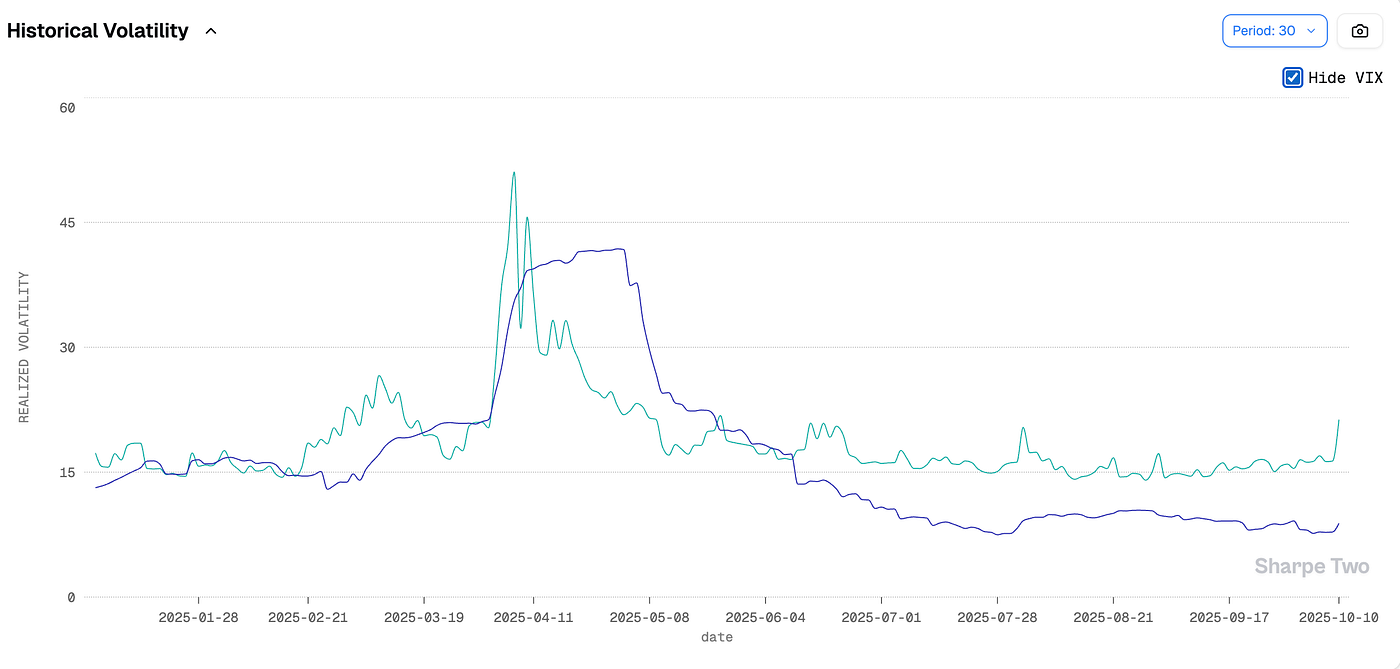

Since May that simple math has been on your side. Realized volatility in U.S. indices has been crushed — single-digit prints in SPX, quiet tapes across sectors — while implieds have refused to come down. The gap between them, the volatility risk premium, has stayed wide.

Since June 2025, the conditions have been perfect for options sellers with implied volatility (in green) constantly outpacing realized volatility (in purple).

That’s why anyone selling short-dated options, running wheels, or writing covered calls has felt like a genius lately. The carry’s been free. Every week you could short the same strikes, collect theta, and watch nothing happen. It’s been the perfect environment for premium sellers: calm realized, sticky implied.

But those are ideal conditions, not permanent ones.

Enjoy the carry while it lasts. Just remember it’s the spread paying you, not the ticker. And spreads don’t stay wide forever.

Betting on your favorite stock every week is no different from betting your football team will win every game. Sometimes you’re right. Most of the time, the odds were fair, and the bookies already priced it in.

That’s the part traders keep missing — there’s no reward for loyalty in a probabilistic game. You’re not being paid to show faith. You’re being paid to find mispricing.

You don’t have to be a quant desk to do it. You just need tools that surface the same signals: when implied volatility runs rich, when the curve kinks, when skew blows out. That’s what professional traders automate — not the trades, but the decision process.

That’s also why we built Sharpe Two — to make that math visible. To give traders without a desk the same view on volatility surfaces, spreads, and setups that actually tilt the odds.

Stop looking for good stocks for premiums. Start trading volatility.