Two weeks ago we were pointing to an opportunity to short volatility in Chinese equities through ASHR. At that moment, the main geopolitical item on our agenda was the state visit of Trump in China at the end of April. And while this is still scheduled, the news headlines are dominated by the war in Iran, started 10 days ago and lacking clarity as to its resolution.

In that context, oil shot up more than 50% in a couple of days, before reverting most of the move so far this week. But realized and implied volatility in many asset classes and geographies have been dragged along for the ride, and ASHR is no exception.

When you are on the short side of volatility you are always at the mercy of these events, and being wrong on a thesis will happen more often than not. What matters is to always control your sizing so that when the unexpected happens, you can weather the storm. But equally important is to focus on areas where the edge is pronounced enough so that even when the unexpected happens, you can land more often than not on the right side of the coin.

And while this quarter is arguably much harder as the volatility from the commodities space is trickling into other asset classes, picking better setups is helping us not dig our own grave. In that sense, while ASHR was originally a winner, things turned quickly in the middle of the trading window. When things calmed down early this week, our position settled and you can now exit at the profit target. Yet another roller coaster, but another example of why the variance risk premium is so persistent over the years: it is not for everyone.

Let’s have a look.

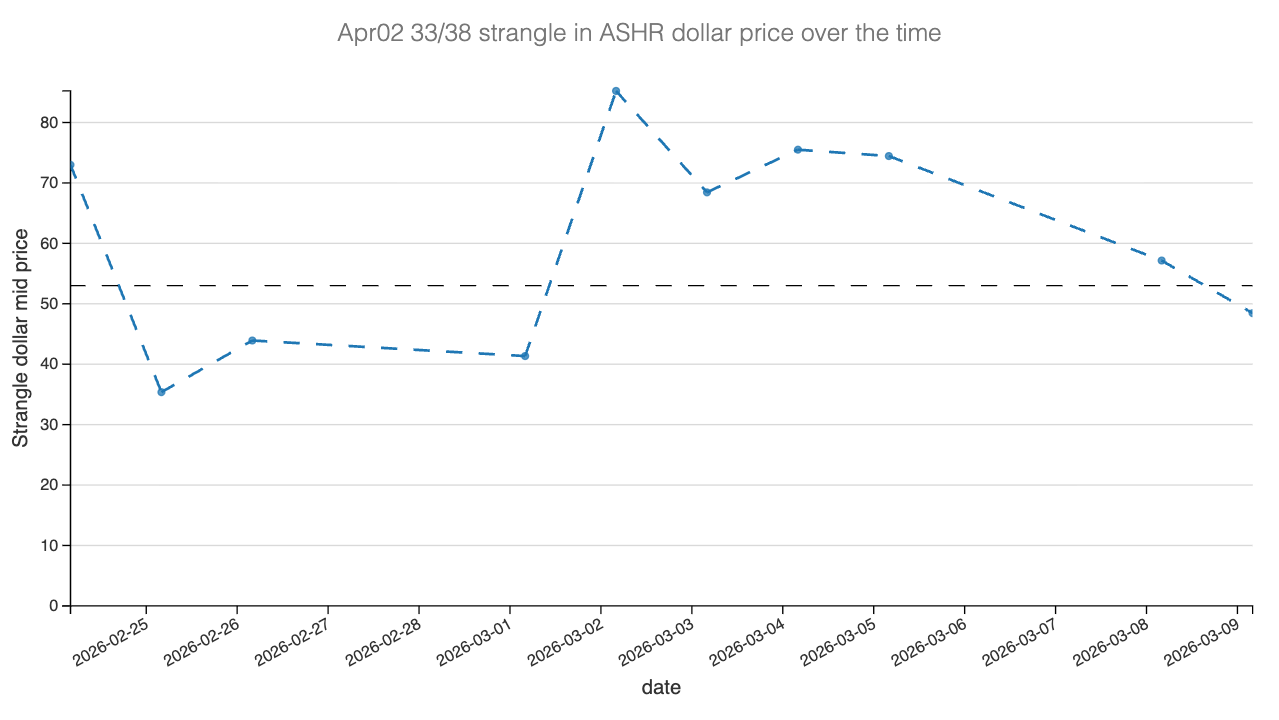

Implied volatility went from tailwind to headwind in a week. The war in Iran repriced everything we had sold.

We were hoping to capitalize on vega, and this would prove to have played against us. What about realized volatility? While at the time of writing, we were pointing to the fact that it could go both ways, it now sits at 16% after the global rout due to the swings in oil prices, as China is quite dependent on imported oil, especially through the Strait of Hormuz.

We are particularly vulnerable to these spikes in realized volatility as we do not delta hedge and in that particular instance, the underlying price lost about 5% in a few days which clearly tested our put strike.

Another clear example that gamma may not always give you the chance to react and sitting too close to the expiration cycle can be particularly detrimental. By focusing on the 30 dte range, we could absorb the vega increase as well as let the underlying settle back as the market adjusted to the developments in the Strait of Hormuz.

With these unexpected circumstances the PnL for the position follows a familiar pattern: an opportunity to take profit really quickly before the trade played against us quite a bit, before ultimately delivering a decent gain.

This highlights what we pointed out in the introduction: having a strong thesis helps weather complicated and unexpected situations. The VRP in ASHR was strong and implied volatility elevated and it is ultimately what offered quick early profit opportunities. And it is also because we had some cushion that we could wake up early March to a position slightly against us. Should you have kept the position after a 5% drop? The only answer for us is what was your pain tolerance? Had you sized too big, we would understand why you would take it off. Otherwise, you could have let the thesis play out for another week.

It is the combination of edge and solid risk management that allows an account to grow over time. Edge without risk management is like driving a Ferrari with no driving skills: a recipe for a disaster. The other side of that story is true: good risk managers do not miraculously become good traders if they do not have edge… one needs to know when to take risk and when to avoid it.

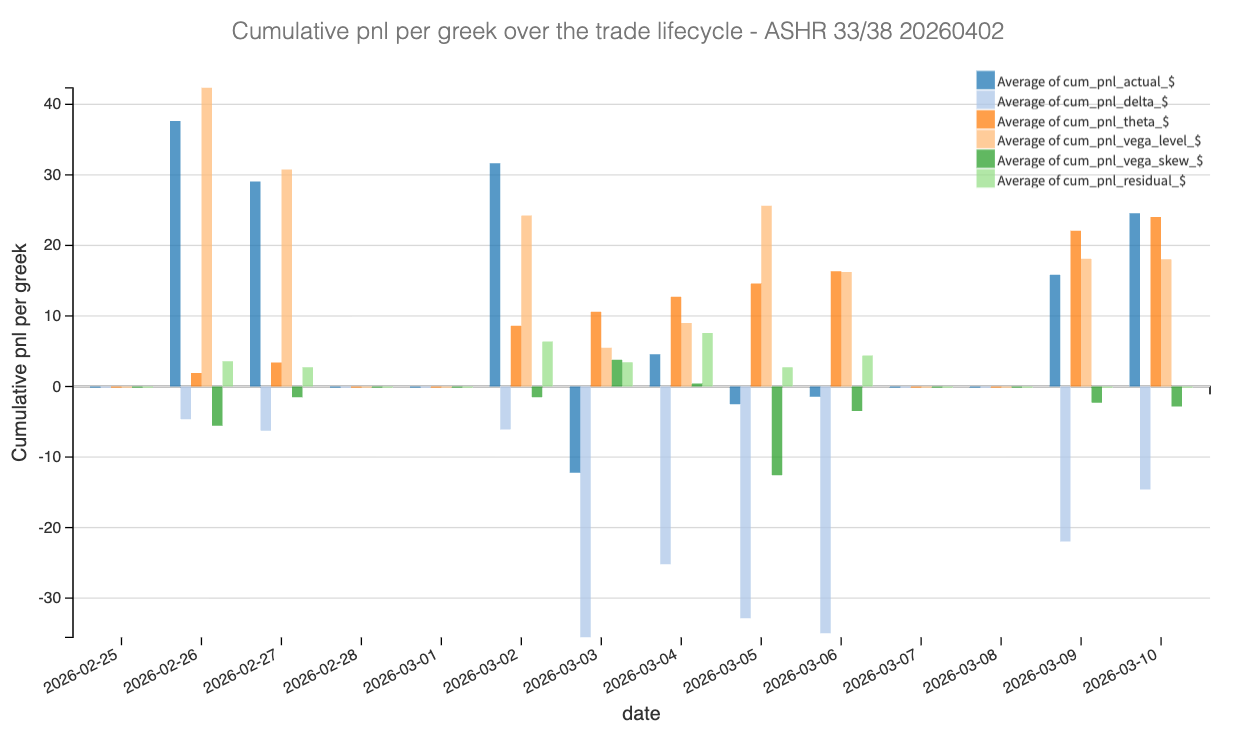

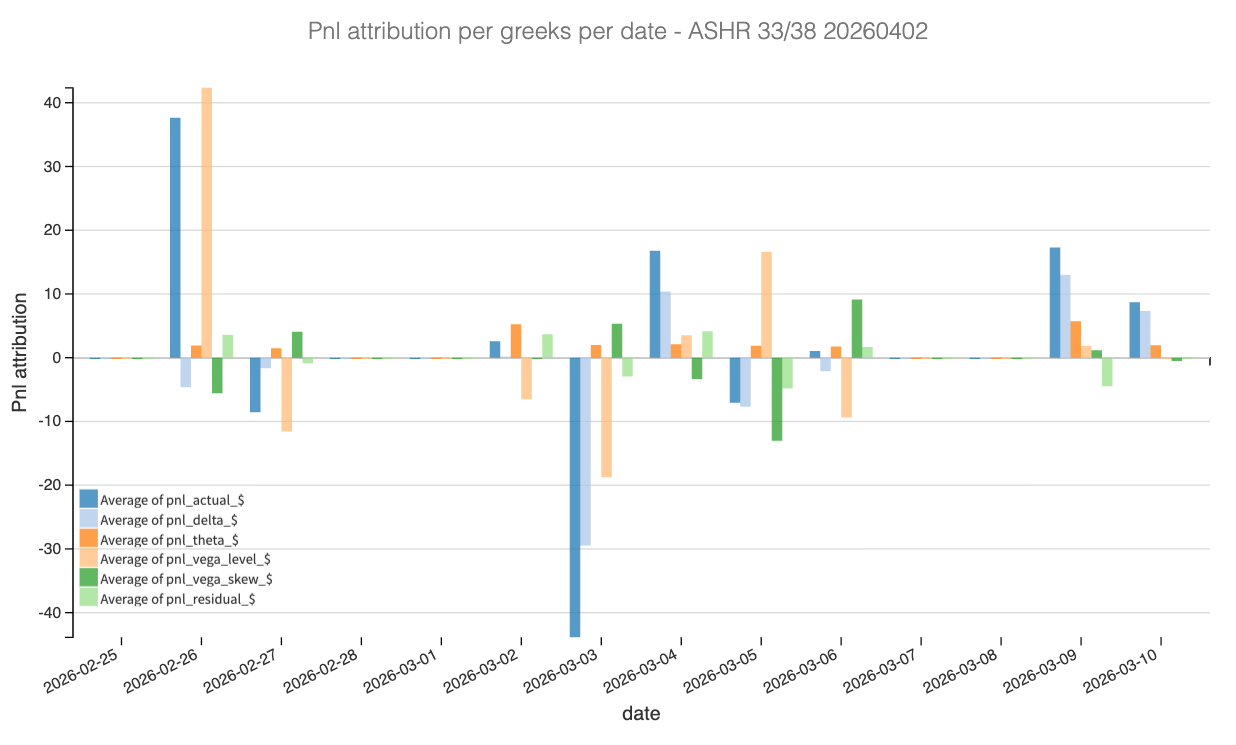

Let’s have a look at the PnL attribution per Greeks now.

The Greeks PnL Attribution

Looking at the attribution, this trade tells the story of a vega tailwind that saved us when delta tried to take it all away while theta that quietly paid the rent throughout.

Theta performed exactly as designed, accumulating $24 over the life of the trade. This is the steady daily income that does not care about the headlines or the Strait of Hormuz: it simply accrues. In a trade where everything else was chaotic, theta was the constant.

The real story was the battle between vega and delta. In the first day after entry, implied volatility compressed sharply — exactly as our model predicted — and vega level surged to +$42, putting the trade in immediate profit. That initial IV compression is what gave us the early exit window some traders could have taken on February 26th.

Then the war erupted. Implied volatility spiked from around 14% back to 19%, and vega level collapsed from +$42 to just +$6 by March 3rd. Simultaneously, the underlying dropped 5% in a few sessions, sending delta to its worst point at −$36. For a brief moment on March 3rd, the trade was underwater at −$12 — a swing of $50 from peak to trough in a single week.

But the thesis held. As the market digested the geopolitical shock and the underlying recovered, delta climbed back to −$15 and vega level stabilized at +$18. Vega skew was a minor headwind throughout, peaking at −$13 on March 5th before settling to −$3. The residual was negligible, confirming that our Greek approximations were accurate.

The mechanical lesson is clear: a 3.6-point VRP cushion at entry was the difference between a loss and a win. Theta generated $24, vega level contributed $18, and even with delta dragging $15, the trade closed at +$25. Edge is not about avoiding storms but building enough cushion to survive them.

Now let’s address the burning question: should we eventually stay in the position or consider recentering it in the monthly April expiry? Let’s have a look.