One of the questions we get asked most often is simple:

What structure should I trade? ATM or OTM? Straddle or strangle? Short or long?

It is a reasonable question. It is also the wrong place to start.

Structure feels actionable, so it becomes the focus. But you can debate strikes endlessly and still have no idea whether you are buying something cheap or selling something expensive.

The only question that matters comes before structure:

- Is the variance implied by the option market overpriced or underpriced relative to what is likely to be realized?

- And more importantly: what is the probability that realized variance will exceed what is currently implied?

That is the question our models at Sharpe Two are built to answer. The problem is that most traders never get to that question, because they start from implied volatility as a number rather than from variance as a process. Most retail traders treat implied volatility as something they read off a screen: IV is 24%, therefore the market is “pricing fear at 24%.” That intuition is often misleading. It comes from a basic misunderstanding of what Black-Scholes-Merton (BSM) is actually doing. In the BSM world, implied volatility is not a measurement. It is an output. A number we back out by forcing a pricing formula to match the option price we already observe. BSM is useful, but it was never meant to describe the full distribution of returns or the market’s expectations about future movement.

It prices one strike, one maturity. A single point in volatility space. If its assumptions held, every strike with the same maturity would imply the same volatility. They do not. We observe smiles, smirks, and skew because the market is pricing risks the model cannot express. So the IV on your screen is not “the market’s expectation of volatility.” It is a convenience variable. If you want to think the way volatility desks think, you stop trading implied volatility and start thinking in variance.

From options to variance

At a structural level, options and variance swaps serve different purposes. An option is an insurance contract against a specific outcome in price space. If the underlying goes above or below a given strike, you are hedged. The exposure is local, tied to point on the price distribution (the strike) and perfectly represented by the volatility surface.

A variance swap hedges something else entirely: the amount of movement the underlying will experience between now and expiration, regardless of direction. Therefore, you can see how options give you local exposure to volatility and how variance gives you global exposure to market’s movement. A variance swap does not rely on a volatility model. Instead, it aggregates information across the entire strip of out-of-the-money options, both puts and calls. The question is no longer “what volatility makes this option price work?”, which is what Black-Scholes answers.

- The question becomes: “what is the market’s aggregate expectation of total movement between now and this maturity?”

That is why institutional desks rarely express volatility views through a single call or put. When they want exposure to volatility itself, they trade variance.

A variance swap is a contract where one party pays a fixed rate and receives the realized variance of the underlying over a period. No strike selection. No directional bias. No local Greeks. Just realized squared movement versus what was implied.

What “model-free” actually means

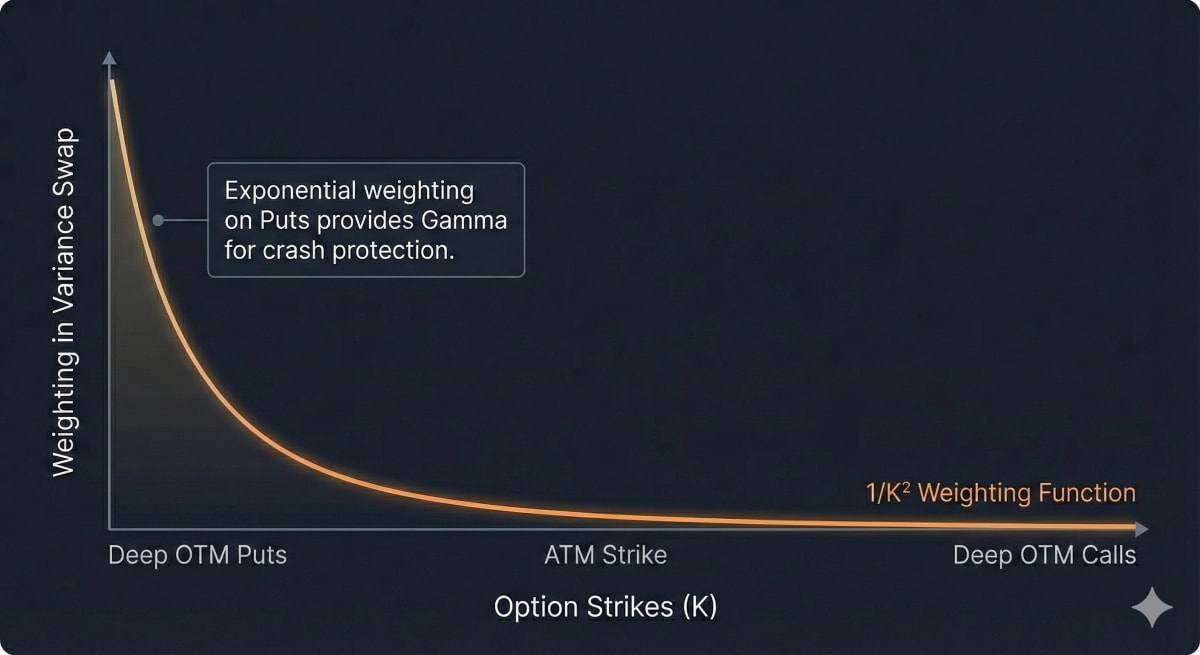

Variance swaps are often called model-free because you do not need to assume a specific dynamics for volatility (constant vol, lognormal returns, etc.) to compute fair variance from option prices like you would in BSM. Instead, fair variance comes from the log contract replication: you integrate a strip of out-of-the-money options across strikes (K) and the weighting looks like 1/K².

Lower strikes get more weight because the curvature of the log payoff explodes as K goes down (variance and volatility tends to increase on the way down).

The market then does the rest: if downside options are rich (equity skew), the put wing contributes more to implied variance. If upside options are rich (call skew), the call wing contributes more.

Let's talk about the VIX for a minute

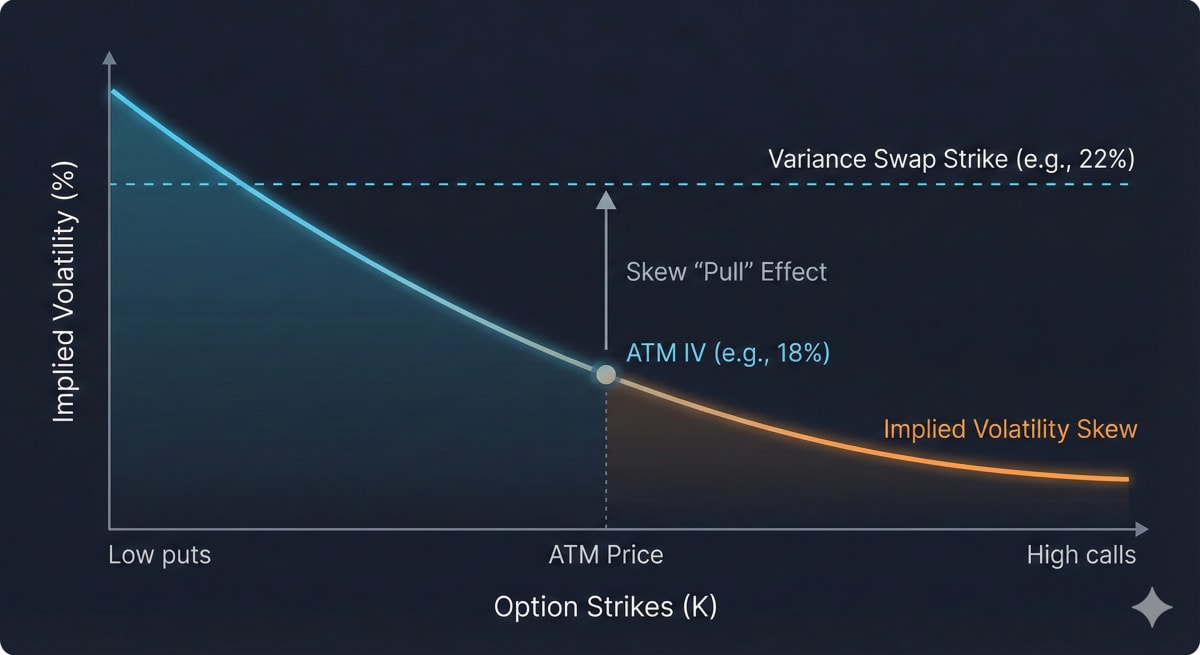

The VIX is simply the square root of a 30-day variance swap on the S&P 500. And because you do not always have a perpetual 30 day to expiration option chain, it is obtained by linearly interpolating between the two option maturities that bracket the 30-day horizon. It is not computed from an ATM straddle and in fact you will often observe the VIX > ATM IV.

Once again that is the artefact of the market pricing downside put more expensive than at the money option.

That linear interpolation matters as it makes the VIX an index and not a directly tradeable object. At any point in time, it represents a moving blend of two different option strips, with weights that change every day. You cannot hold that exact basket dynamically without constant time rebalancing. This is why unlike popular belief, you cannot trade spot VIX itself.

Trading variance is not trivial either. A true variance swap requires exposure to the entire OTM option strip, weighted by 1/K², and dynamically delta-hedged over time. Operationally, that means many legs, wide spreads, and continuous management.

For retail traders, this is impractical.

The CBOE has introduced variance futures (VA), which move closer to what institutional desks trade with one another. But even then, the product set is limited. What if you want variance exposure on QQQ? Or TLT? Or a single stock?

So the real question becomes: how do you approximate global variance exposure with a small number of strikes, in a way that is actually tradable?

How to approximate a variance swap as a retail trader

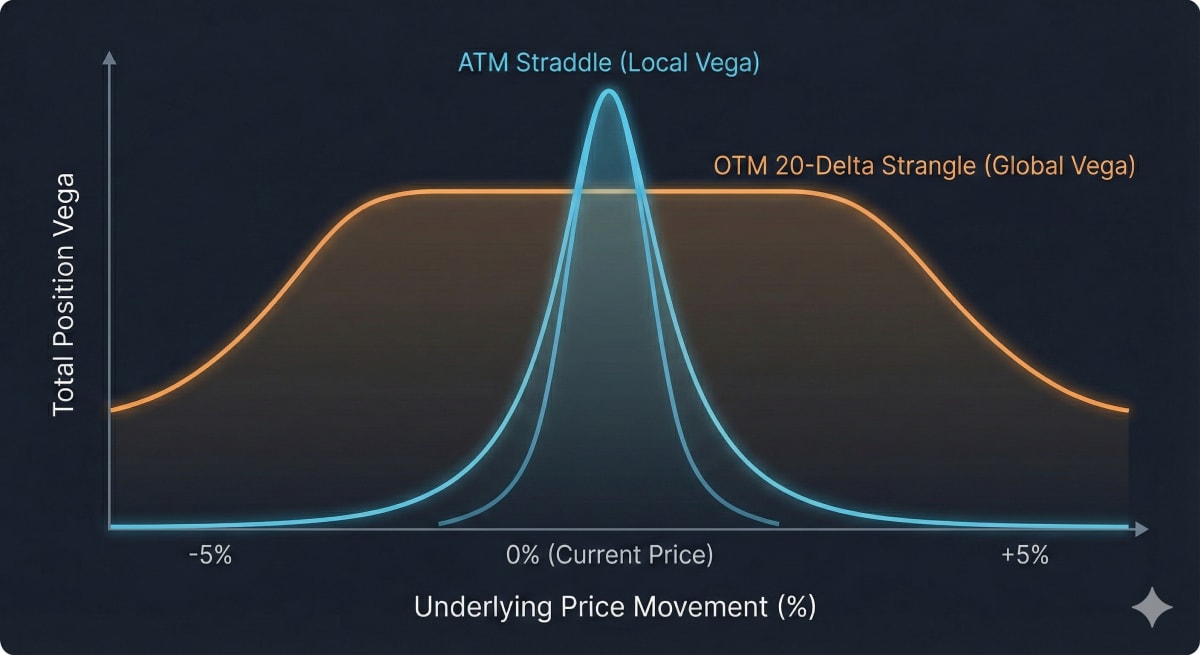

The ATM straddle is the default retail answer to “volatility exposure.”

The problem is that an ATM straddle is a local object. Its vega and gamma profile changes fast as spot moves away, which makes the P&L highly path-dependent. If you are short an ATM straddle, you are not only saying “realized variance will be low.” You are also saying “spot will not travel far from the money while I hold this.” In the wrong regime, that is a strong assumption.

A variance swap does not care about the path. It cares about total squared movement.

So an ATM straddle is not wrong. It is just not a good proxy for variance.

Because the replication of variance uses a 1/K² kernel, implied variance is typically pulled away from the money. In equity underlyings with negative spot/vol correlation, that pull is usually dominated by the downside: a large share of priced variance sits in the 10–30 delta region, where skew lives and crash insurance is actually being bought.

So the real question is practical: how do you get closer to “global variance” with a small number of legs?

You cannot trade a true variance swap as a retail trader. But you can bias your exposure toward where variance is priced, instead of concentrating it at one point.

If you had to pick only two legs, our go to would be to target a 20 delta strangle.

A slightly more sophisticated approach is to distribute long vol across the surface:

- One mid-delta strangle (around 25–30 delta) to anchor exposure

- One lower-delta strangle (around 10–20 delta) to add convexity

This does two things.

First, it broadens your gamma and vega footprint. As spot moves, different legs take turns carrying the exposure. Your sensitivity rolls instead of collapsing.

Second, it naturally respects skew. And if you want to be closer to how variance is actually weighted in equity indices, you can overweight the put side to reflect downside asymmetry.

One precision point: this is not a variance swap. It is not a replication. It is a structural bias toward global variance rather than local volatility.

That distinction matters, because it is also where Sharpe Two fits. Our models are built to answer a simple question: given the surface today, is the variance being sold or bought expensive, and what is the probability that subsequent realized volatility exceeds what is currently implied?

Final thoughts

The real shift is not the structure but the question you ask.

Stop asking where is the stock going or what is the IV of this strike? Instead you should wonder if the market underpricing or overpricing total movement across the entire distribution?

Black-Scholes is a pricing tool. It was never meant to describe reality. Model-free variance is closer to that reality. It is what the market actually charges for movement and uncertainty.

Once you internalize this, you stop trading opinions about direction and start trading distributions of outcomes.

That change in perspective is subtle, but it is the difference between retail intuition and professional volatility thinking.