There is a question that surfaces regularly in our Discord and across every options selling community we follow: why does my iron condor win 70% of the time but barely make money?

The usual suspects get blamed. Poor timing, wrong strike selection, not managing winners fast enough. And sure, those matter. But they are not the real problem.

The real problem is structural. It starts with what you are actually trading when you sell options based on implied volatility signals.

Our probability models at Sharpe Two are built on model-free implied volatility. This is not the Black-Scholes implied vol you see on a broker screen. It is a measure of the market's total expected variance, extracted from the full option chain across all strikes. When our VRP signal reads SHORT, what it is really saying is: the market is pricing in more variance than is likely to realize. The theoretically correct instrument to capture this is a variance swap: you sell variance at the implied level and settle against realized. Clean, direct, no strike selection required.

But retail traders cannot trade variance swaps and often the closest approximation is a short strangle, specifically around the 20-delta level, where the combination of put and call replicates the variance swap payoff more faithfully than any narrow-strike position. The key is that you need exposure across the full distribution of outcomes, including the tails. A 20-delta strangle gives you that.

An iron condor does the opposite. It takes that variance exposure and amputates the tails by buying wings at the same expiry. And those tails (the deep out-of-the-money puts in particular) are exactly where the richest variance premium lives.

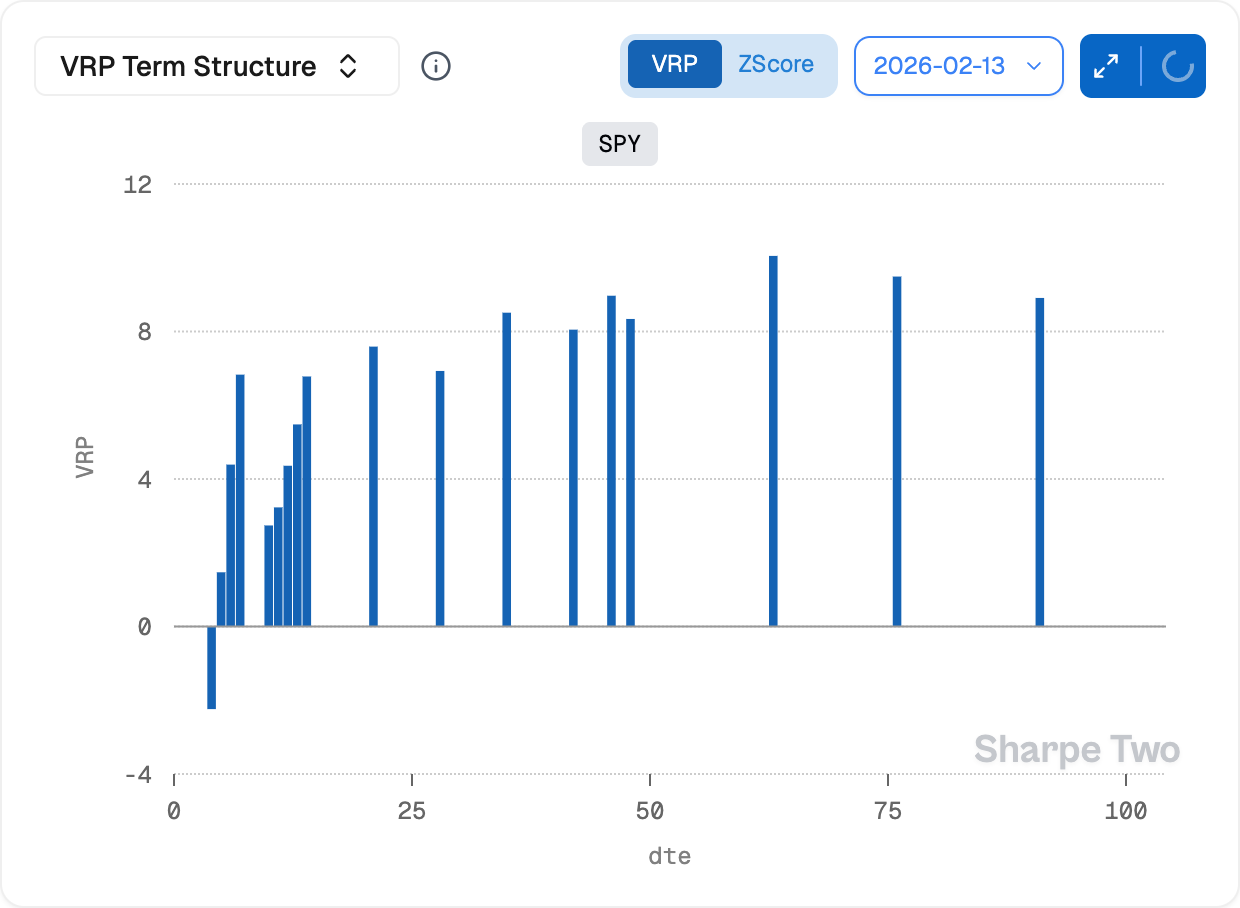

Right now, SPY's variance risk premium sits at 8.51 points at 35 days to expiry, with a z-score of 1.64. Our 30-day VRP signal reads SHORT at 71%. This is a strong environment for selling variance. But if you are selling it through an iron condor, you are giving back a meaningful portion of what the market is handing you.

Let's have a look.

Where VRP Actually Lives

The variance risk premium is not evenly distributed across the vol surface. It concentrates in specific places, and understanding where changes everything about how you structure a trade.

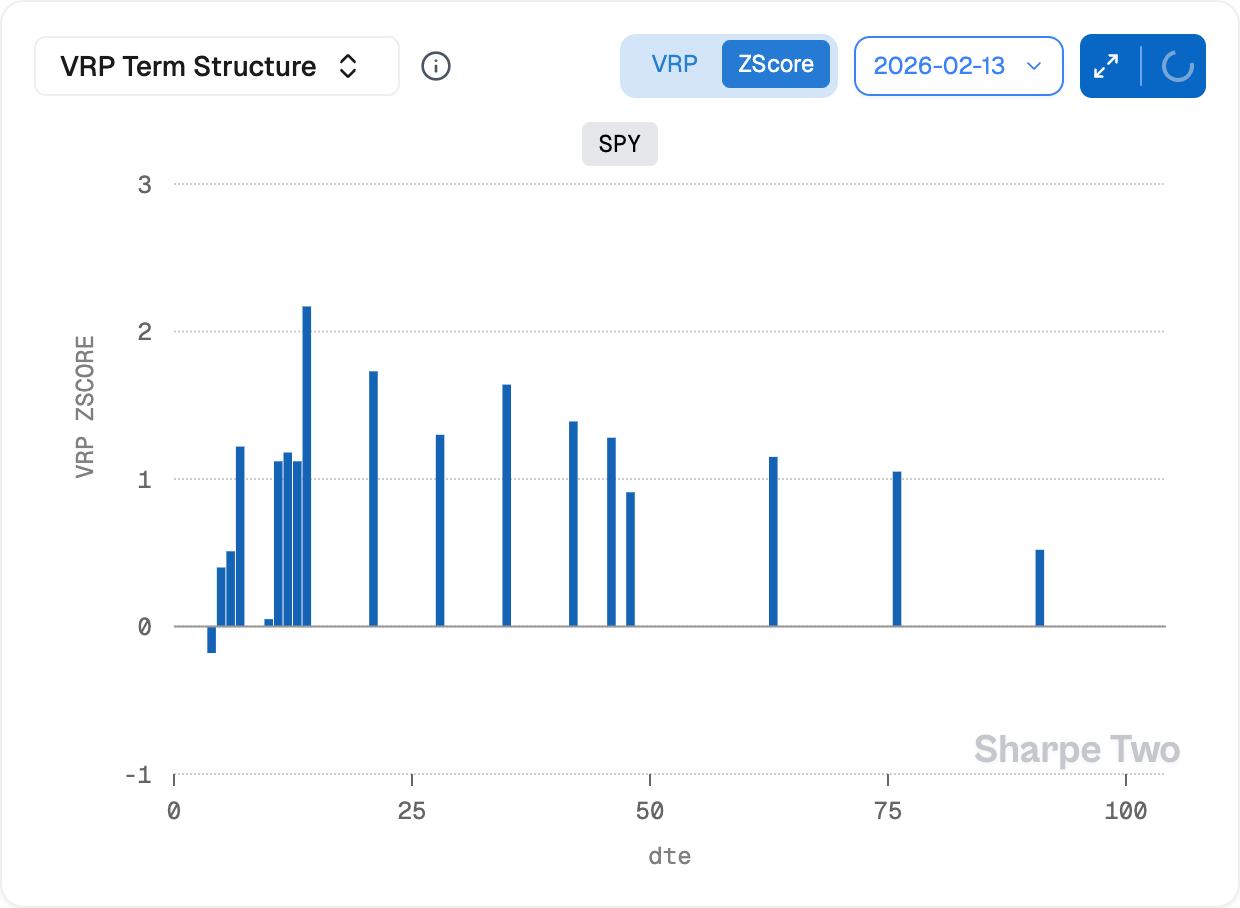

Start with the term structure. At 4 days to expiry, VRP is actually negative: implied volatility at 13.60% sits below realized at 15.85%. The market is underpricing near-term risk. But move out to 14 DTE and VRP jumps to 6.78 with a z-score of 2.17 or the highest on the curve. At 35 DTE it reaches 8.51 (z=1.64). At 63 DTE, it peaks at 10.05 points.

In absolute terms, VRP rises with tenor right now. But this is not always the case. Back-month options often carry less embedded risk premium than the front, because they lack the structural hedging flow that inflates near-term put prices. The normal VRP term structure slopes downward: richest at the front, thinner further out. The current upward slope is an exception, not the rule and the z-scores tell a more reliable story: at 14 DTE the z-score is 2.17, the highest on the curve, even though absolute VRP is only 6.78. The sweet spot sits between 14 and 42 DTE, where VRP is most anomalous relative to its own history.

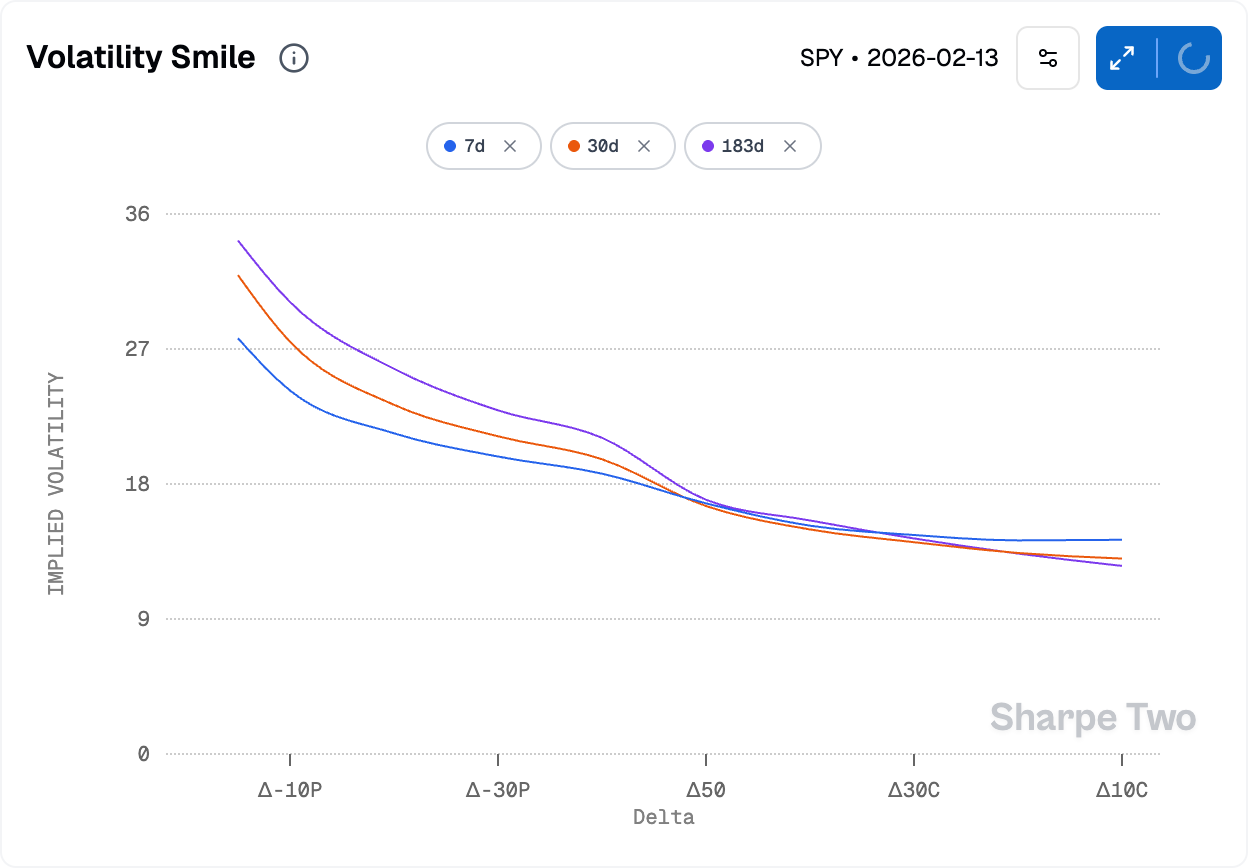

But tenor is only half the picture. VRP also concentrates by strike. Carr and Wu demonstrated this in their 2009 paper in the Review of Financial Studies: the variance risk premium is disproportionately embedded in out-of-the-money puts. The options that carry the most edge are the ones furthest down the put skew... exactly the ones an iron condor buys back as wings.

We can see this directly in the current SPY options chain. On the March 20 expiry (32 DTE), the skew steepens dramatically as you move down the delta ladder:

The 15-delta put at 24.50% implied vol and the 5-delta put at nearly 32% are the most expensive options in the entire chain. They carry the highest embedded risk premium. And when you put on an iron condor, you buy them.

Let’s now consider this concrete example: A 20-delta strangle on SPY where you sell the 645 put at $5.50, sell the 707 call at $3.21 gets you $8.71 in total credit. Now add wings:

- Tight IC (15-delta wings): buy the 633 put at $3.84, buy the 712 call at $2.23. Wing cost: $6.07. Net credit: $2.64. You surrendered 70% of the premium.

- Wide IC (5-delta wings): buy the 585 put at $1.13, buy the 725 call at $0.89. Wing cost: $2.02. Net credit: $6.69. You surrendered 23% of the premium.

The tight IC gives back $6.07 of the $8.71 and $3.84 of that goes to buying the 633 put at 24.50% implied vol, the single richest option relative to likely realized vol on the entire surface. You are paying for insurance denominated in your own edge, and the exchange rate is terrible.

The Evidence: 100,000 Paths

Enough with the theory and let’s run some numbers.

Using a Heston stochastic volatility model calibrated to current SPY dynamics ( starting variance at 13.44% annualized (current 30-day realized), with mean reversion, vol-of-vol at 0.4, and a -0.70 spot-vol correlation) we simulated 100,000 paths over 32 days to the March expiry. We tested four portfolios, all built on the same 20-delta short strangle:

Read the tight IC column carefully. A 68.6% win rate sounds reasonable but the mean P&L is $0.45 per contract on a trade that ties up $9.36 in margin for a month. It wins often, it wins small, and when it loses it loses the maximum every time. This is the iron condor trap: the win rate flatters, the expected value does not.

And in this environment, even the win rate is unimpressive. VRP is at a z-score of 1.64 and the premium is rich. The naked strangle wins 77.6% of the time precisely because it captures that edge fully. In a flatter or outright negativeVRP environment, the strangle's win rate would compress and the IC's defined risk might offer a reasonable tradeoff. But why would you trade the VRP in such a regime ….?

When you know the premium is this rich, the iron condor gives you the worst of both worlds: it caps your upside at $2.64 while barely improving win rate over the unhedged position.

The wide IC does better ($1.50 mean P&L) but look at its tail risk. The 1st percentile is -$48.87, nearly identical to the naked strangle's -$49.02. When the move is large enough to breach the 20-delta short strike, a 5-delta wing 60 points further out does almost nothing to help. You paid $2.02 for protection that activates only in the most extreme scenarios and still leaves you with a $53 max loss.

Now look at portfolio D, the cross-expiry hedge. This is a naked 20-delta strangle with 10-delta wings bought in the May expiry (88 DTE), not the March. The net credit is only $2.07, but the mean P&L is $2.08, nearly matching the naked strangle's $2.71. And the tail risk is materially better: the 1st percentile improves from -$49.02 to -$25.39. The worst path drops from -$161.28 to -$48.93.

Why does this work? Because the May wings still have 56 days of life remaining when the March strangle expires. In calm markets, they retain time value and decay slowly. In a crash, they benefit from both intrinsic value and a vol spike: the Heston model's spot-vol correlation drives variance higher when the spot drops, inflating the remaining wings.

The best path for portfolio D is +$42.02, far beyond the $8.71 cap of the naked strangle. That number deserves explanation. The scenario is a sharp mid-period selloff (think August 2024) where realized variance spikes to several multiples of its starting level. Crucially, spot then mean-reverts and finishes between the short strikes at March expiry. The strangle expires worthless, keeping the full $8.71 credit. But the May wings, repriced at dramatically elevated implied volatilities with 56 days of life remaining, are now worth far more than their $6.64 entry cost. You capture both the premium on the front-month strangle (although arguably, the thesis to be short vol was wrong at the first place…) and the convexity payoff from the back-month wings. It requires vol to spike and spot to recover but when it happens, you get paid on both legs.

One practical note: at March expiry, the May wings still have 56 days of life. You will need to either close them, roll them into a new front-month strangle, or let them decay. The trick is often to realize that at that stage, these wings have been partly paid off: if you keep them, the front month trade has allowed you to keep them at a significant discount compared to the current market price…

What to Do Instead

The simulation helps us have the full picture: trading variance and with a 20 delta strangle is a good approximation of the the variance-swap logic in practice. The iron condor however, removes tail exposure from the same expiry and fights the structure of the trade. The cross-expiry hedge preserves the front-month variance capture and buys protection where it is cheaper: further out in time, where VRP z-scores are lower and the insurance is less overpriced.

If you have the capital, the naked strangle captures the most edge per contract, the full variance risk premium but the tail risk is real: -$161 in the worst simulated path. This is not a trade for small accounts or light risk tolerance.

If you want protection, buy it in a different expiry. The cross-expiry hedge (selling the front month, buying wings in the back month) delivers 77% of the strangle's expected value while cutting the 1st percentile loss nearly in half. The key insight is that back-month wings are cheaper in VRP-adjusted terms. At 88 DTE, the VRP z-score is 0.52 versus 1.64 at 35 DTE. You are buying insurance where it is least overpriced.

The signals confirm the environment. Our 30-day VRP signal reads SHORT at 71%, implied vol direction is SHORT at 70%, and skew is SHORT at 89% , the strongest reading in the set, suggesting the put skew is likely to compress. When the environment is this favorable for selling variance, every point of edge you surrender to an iron condor wing matters more.

Now, let us be honest about the constraint that makes iron condors exist in the first place: margin. A 20-delta strangle on SPY requires roughly $16,600 in portfolio margin, a meaningful capital for a single position. The iron condor solves this by capping the margin requirement at the wing width. For a $25,000 Reg-T account, that may be the only way to participate.

We do not fault anyone for trading iron condors when capital constraints demand it. But we do ask this: understand what you are giving up. The defined risk of an IC is not free. It comes at the cost of surrendering the richest premium on the volatility surface, the out-of-the-money put skew that accounts for a disproportionate share of the variance risk premium. If you must trade an IC, widen those wings as far as margin allows. Although, we hope we managed to convince you that a cross expiry hedge is often the best of both world.

The question is not whether iron condors are bad trades. It is whether you know what they cost you.